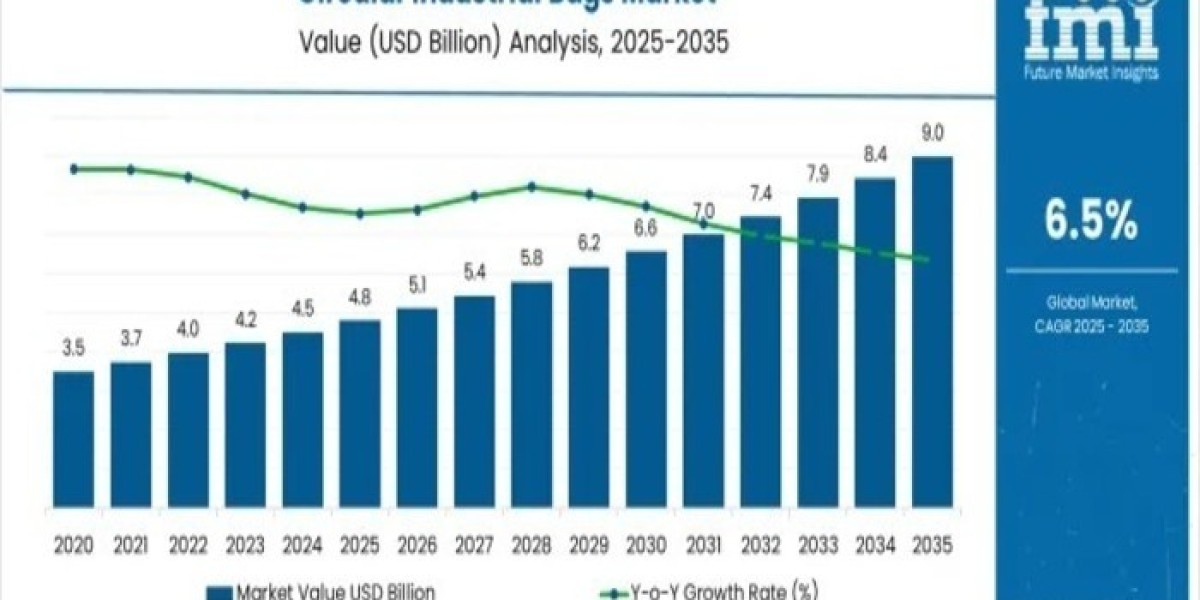

The global Circular Industrial Bags Market is entering a decade of significant transformation. Valued at USD 4.8 billion in 2025, the market is projected to reach USD 9.0 billion by 2035, growing at a CAGR of 6.5%. This strong upward trajectory reflects the increasing shift toward sustainable, durable, and efficient industrial packaging solutions.

Circular industrial bags also known as tubular flexible intermediate bulk containers (FIBCs), are witnessing rising adoption across industries such as food, agriculture, construction, and chemicals due to their superior strength, reusability, and cost-effectiveness.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates – https://www.futuremarketinsights.com/reports/sample/rep-gb-8788

Meaning and Definition

Circular industrial bags are heavy-duty packaging solutions made using woven fabric on circular looms, giving them a tubular structure without side seams. This design enhances strength and load-bearing capacity, making them ideal for storing and transporting bulk materials such as grains, fertilizers, powders, and chemicals.

Available in coated and uncoated variants, these bags can be fitted with valves or spouts for efficient filling and discharge. Their high tensile strength, moisture resistance, and recyclability make them one of the most preferred industrial packaging formats worldwide.

Market Overview

Circular industrial bags offer an optimal combination of strength, efficiency, and sustainability. Their ability to handle powdered and hygroscopic materials has made them indispensable in industries such as milling, sugar processing, animal feed, and construction. Unlike traditional packaging options like cartons or metal drums, circular bags reduce packaging weight and enhance operational efficiency during storage and transit.

From the standpoint of industrial packaging, these bags stand out for their structural integrity and space optimization allowing for stable stacking, uniform load distribution, and reduced product damage. The market’s expansion is underpinned by advances in polymer fabric technologies, enabling better tensile strength and environmental resistance while supporting circular economy goals.

Market Outlook (2025–2035)

The Circular Industrial Bags Market is on a steady upward trajectory, driven by the convergence of industrial modernization, sustainability initiatives, and bulk material handling needs. Rising industrialization in Asia-Pacific, coupled with stringent waste management and sustainability regulations in North America and Europe, is creating fertile ground for market expansion.

By 2035, the market will nearly double in size, supported by demand from food, construction, and chemical sectors, where packaging safety, hygiene, and efficiency are paramount. The transition to recyclable polypropylene-based bags and the use of automated filling systems are further enhancing the market’s operational appeal.

Growth Drivers and Demand Factors

- Sustainability and Waste Reduction – The global focus on reducing plastic waste and promoting recyclable materials has accelerated the adoption of polypropylene-based circular bags.

- Industrial Expansion – The rise of bulk handling in agriculture, construction, and chemicals is fueling demand for durable, reusable packaging solutions.

- Advancements in Fabric Technology – Improved weaving and lamination techniques are producing bags that can endure higher stress, moisture, and UV exposure.

- Operational Efficiency – Lightweight and easy-to-handle designs reduce shipping costs and enhance warehouse space utilization.

- Stringent Regulations – Increasing environmental compliance requirements are pushing industries to opt for recyclable, long-lasting packaging alternatives.

Segmental Insights

- By Fabric Type: The Polypropylene (PP) segment dominates with a 30% market share in 2025, driven by its superior strength-to-weight ratio, cost efficiency, and chemical resistance. PP’s adaptability to various lamination techniques further strengthens its appeal for industrial applications.

- By Product Type: The Flat Bottom design leads with a 45% share, owing to its stability and stacking efficiency. These bags allow for better load management and automation compatibility, making them the preferred choice in large-scale industrial storage and transport systems.

- By End-Use Industry: The Food Industry accounts for 25% of the market share in 2025, reflecting the growing need for safe, contamination-resistant packaging for grains, sugar, and flour. Food manufacturers prefer circular bags for their hygiene standards, moisture resistance, and ease of handling.

Regional Landscape

- Asia-Pacific leads the global market, with China (8.8% CAGR) and India (8.1% CAGR) emerging as the fastest-growing countries. Expanding industrial sectors and infrastructure development projects are propelling regional demand.

- Europe remains a key hub for sustainable packaging, with Germany (7.5% CAGR) at the forefront, driven by advanced manufacturing and recycling capabilities.

- North America, led by the USA (6.2% CAGR), continues to adopt innovative packaging technologies in chemicals, agriculture, and food sectors.

- Japan and South Korea show stable growth, supported by technological innovation and strict packaging quality standards.

Emerging Trends

- Recyclable and Bio-based Materials: Manufacturers are increasingly investing in recyclable and bio-based polymer alternatives to meet green packaging mandates.

- Automation and Smart Filling Systems: Integration of automation in filling and discharge systems is enhancing efficiency in packaging lines.

- Customization and Branding: Industries are demanding printed, color-coded, and custom-sized circular bags to align with brand identity and operational needs.

- Digital Monitoring and RFID Integration: Smart tagging and tracking technologies are being adopted to monitor bag usage, lifecycle, and logistics flow.

Competitive Landscape

The market is moderately consolidated, with key players such as Berry Plastics, Global-Pak, BAG Corp, Greif, Conitex Sonoco, AmeriGlobe, and LC Packaging dominating global supply. These players are focusing on product innovation, material recycling, and regional expansion to maintain a competitive edge. Collaborations, mergers, and technology integration are central to their growth strategies.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.