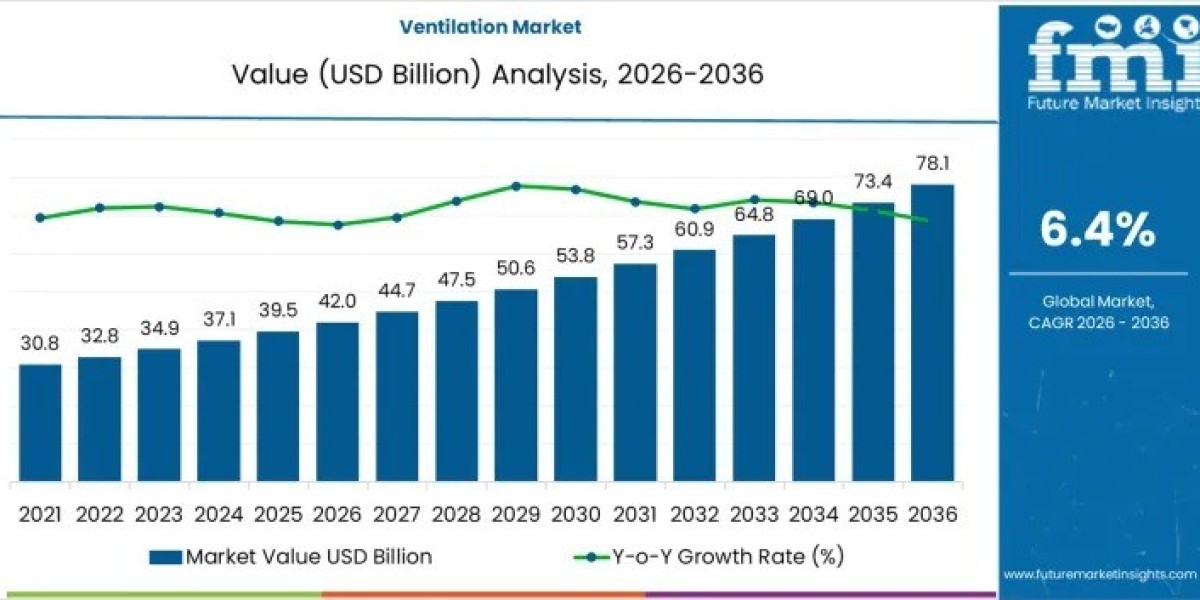

The global Ventilation Market is forecast to expand from USD 42 billion in 2026 to USD 78 billion by 2036, registering a CAGR of 6.4%. This growth is not merely a function of construction volume but reflects how buildings are designed, regulated, and operated. Ventilation is now a measurable contributor to indoor air quality (IAQ), energy efficiency, and occupant well-being. As a result, suppliers with engineering ownership over fan design, motors, and control electronics retain greater pricing power than assemblers dependent on third-party components.

Key Market Signals

- Market value increases by USD 36 billion between 2026 and 2036

- Growth is specification-led rather than shipment-led

- Integrated manufacturers capture higher margins through compliance-driven demand

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates:

https://www.futuremarketinsights.com/reports/sample/rep-gb-31015

Cost Structures and Margin Dynamics Shape Competitive Positioning

Cost structures vary significantly across the ventilation industry due to differences in sheet metal fabrication, motor sourcing, electronics integration, and installation complexity. These variations influence competitive positioning more than unit volumes alone. Manufacturers that internalize engineering and production control benefit from stable margins, while component-dependent players face input cost volatility and margin pressure.

Profitability Insights

- Large commercial and infrastructure projects support stable margins

- Residential and light commercial segments remain price-sensitive

- Services, retrofits, and control upgrades deliver higher-margin revenue

- Logistics and working capital efficiency affect realized profitability

Despite steady market expansion, operating profits remain concentrated among firms with strong specification influence and integrated manufacturing capabilities.

Growth Outlook Through 2036: From Volume to System Value

Between 2026 and 2031, the market grows along a 6.4% CAGR trajectory, driven by stricter building codes, green certifications, and rising IAQ awareness. Commercial buildings, healthcare facilities, and large residential projects lead demand as buyers evaluate lifecycle energy use, noise levels, and controllability.

From 2031 to 2036, growth increasingly comes from refurbishment and optimization rather than new floor space additions. Ventilation systems become more tightly integrated with HVAC and energy management platforms, raising system value per project even when physical scale remains unchanged.

Growth Drivers by Phase

- 2026–2031: Code compliance, IAQ standards, retrofit demand

- 2031–2036: Operational efficiency, monitoring, system integration

Mechanical Ventilation Dominates System Adoption

Mechanical ventilation accounts for approximately 46% of global demand in 2026. Its dominance reflects the need for predictable, controllable air exchange independent of climate conditions. Mechanical systems enable filtration, heat recovery, zoning, and time-based airflow control, making them essential for dense urban buildings and sealed envelopes.

Why Mechanical Systems Lead

- Guaranteed airflow and filtration performance

- Compliance with fixed IAQ standards

- Suitability for commercial, healthcare, and high-occupancy buildings

Natural, hybrid, and exhaust-only systems address niche requirements but lack the consistency required for most regulated environments.

Residential Buildings Anchor Market Volume

Residential construction represents around 41% of ventilation demand in 2026. Urbanization, apartment construction, and tighter building envelopes increase reliance on planned ventilation rather than passive air leakage. Building codes increasingly mandate minimum ventilation rates in homes, sustaining unit demand across both new construction and retrofits.

End-User Demand Patterns

- Residential: High volume, smaller system size

- Commercial: Lower volume, higher system complexity

- Industrial & healthcare: Regulation-driven, high value per project

Regional Growth Reflects Urbanization and Regulation

Growth varies by region based on construction activity and regulatory pressure:

- India: 7.2% CAGR driven by urbanization and healthcare expansion

- China: 7.0% CAGR supported by industrial growth and air quality rules

- Brazil: 6.3% CAGR from infrastructure modernization

- USA: 6.0% CAGR linked to system upgrades and smart buildings

- UK: 5.8% CAGR reflecting retrofit activity and energy efficiency goals

Competitive Landscape Defined by Integration and Reliability

Competition centers on airflow efficiency, energy performance, control integration, and durability. Leading players include Daikin Industries, Carrier Global Corporation, Johnson Controls, Lennox International, Panasonic, Systemair AB, and Greenheck Fan Corporation. Differentiation increasingly comes from digital controls, monitoring capabilities, aftermarket services, and regulatory compliance.

Ventilation Transitions to a Managed Performance System

The market is shifting from static airflow sizing to performance-based ventilation. Sensors, variable airflow systems, and real-time monitoring allow ventilation to respond dynamically to occupancy and air quality. Regulations are becoming outcome-focused, reinforcing ventilation as an actively managed building system rather than hidden infrastructure.

By 2036, continuous performance verification, energy impact management, and documented IAQ outcomes are expected to define supplier success.