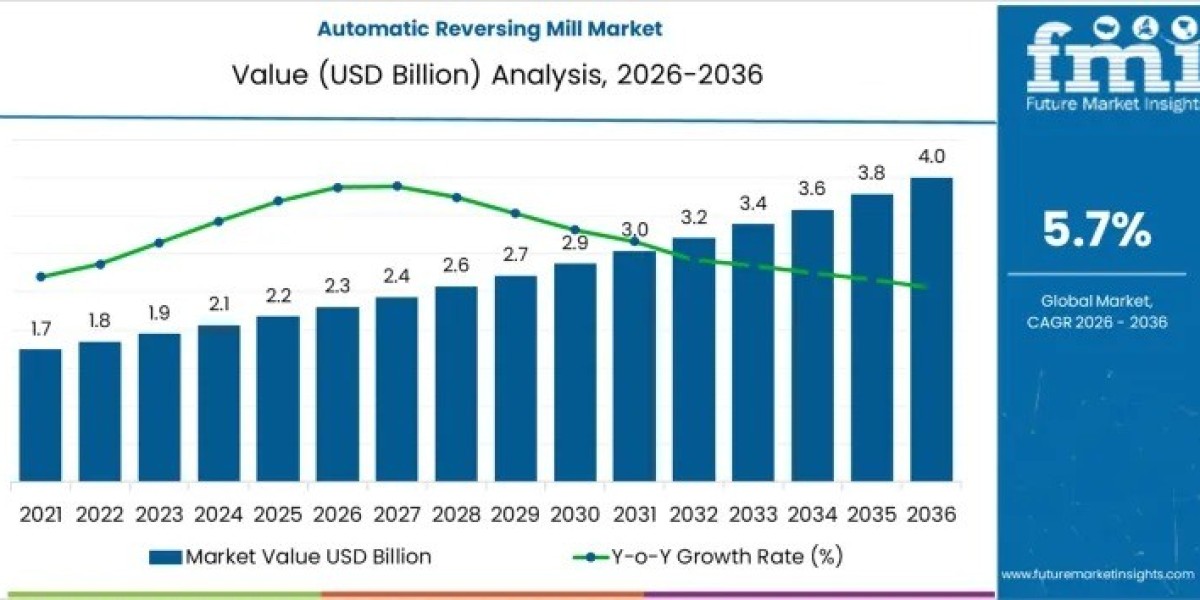

The Automatic Reversing Mill Market is transitioning from volume-driven expansion to value-led growth as steel and non-ferrous producers intensify focus on automation depth, operating efficiency, and lifecycle economics. The market is forecast to grow from USD 2.3 billion in 2026 to USD 4.0 billion by 2036, expanding at a CAGR of 5.70%. Growth momentum is supported by modernization of aging rolling infrastructure, rising demand for precision-rolled metal products, and increasing adoption of digital control systems.

Request For Sample Report | Customize Report | Purchase Full Report –

https://www.futuremarketinsights.com/reports/sample/rep-gb-31289

Key Market Growth Metrics

- Market Value (2026): USD 2.3 Billion

- Forecast Value (2036): USD 4.0 Billion

- CAGR (2026–2036): 5.70%

- Leading Mill Type: Two-Stand Reversing Mills (48% share)

- Major Growth Regions: Asia Pacific, Europe, North America, Latin America, Middle East & Africa

Why the Automatic Reversing Mill Market Is Expanding

Growth is anchored in rising demand for high-precision rolling equipment across steel, aluminum, and specialty metal processing. Automatic reversing mills enable flexible thickness control, improved surface quality, and efficient slab and plate processing, making them suitable for both primary and secondary production facilities.

Additional growth drivers include:

- Modernization of legacy rolling mills to reduce manual intervention

- Integration of automation and digital monitoring to improve yield and reduce scrap

- Energy efficiency mandates pushing adoption of advanced drive and control systems

- Infrastructure development and industrialization in emerging economies

Value Shift Toward Automation and Lifecycle Services

Between 2026 and 2036, competitive performance is shaped less by shipment volumes and more by pricing power and service intensity. Capital expenditure remains front-loaded, with mill stands, drives, and automation representing the largest cost components. Suppliers bundling proprietary automation, control software, and modernization packages are capturing stronger margins.

Key value capture trends include:

- Shift from hardware-only sales to integrated automation platforms

- Expansion of lifecycle services, upgrades, and digital optimization tools

- Higher switching costs strengthening supplier pricing leverage

- Margin pressure on vendors lacking automation IP

Segment Analysis: Type and Application

By Type

Two-stand reversing mills lead the market with 48% share, offering an optimal balance between flexibility and investment efficiency. These mills support frequent grade changes, diversified production schedules, and lower maintenance complexity.

Other segments include:

- Four-stand reversing mills for higher rolling loads

- Six-stand reversing mills for precision-intensive applications

By Application

Automotive steel processing dominates with 41% share, driven by demand for flat steel products with tight dimensional tolerances.

Key application drivers include:

- Vehicle body panels and chassis components

- High-strength steel for safety and structural parts

- Growing electric vehicle production requiring specialized steel grades

Regional Outlook Highlights

- China: CAGR 6.3% (2026–2036), driven by modernization and efficiency upgrades

- India: CAGR 6.8%, supported by new steel capacity additions and infrastructure growth

- USA: CAGR 4.6%, largely replacement-driven modernization

- Germany: CAGR 4.3%, focused on precision and efficiency upgrades

- Japan: CAGR 3.9%, reflecting mature industrial base and selective refurbishment

Asia Pacific remains the primary growth engine, while North America and Europe exhibit steady, value-oriented expansion.

Technology Trends Reshaping the Market

Technological advancement is redefining competitive positioning in the automatic reversing mill market.

Key technology trends include:

- PLC-based and AI-driven control systems for rolling accuracy

- Digital twin applications for pass simulation and parameter optimization

- Energy-efficient drives and regenerative braking systems

- Advanced hydraulic controls to reduce power consumption

These innovations enhance throughput, stabilize quality, and lower operating costs.

Competitive Landscape and OEM Strategies

Leading players such as ANDRITZ AG, SMS group GmbH, Primetals Technologies, Danieli, Tenova, and John Cockerill Group are competing through automation depth and lifecycle efficiency rather than price. Mid-sized suppliers differentiate via niche applications, compact layouts, and precision-focused designs. Brochure-backed performance metrics and service offerings increasingly influence procurement decisions.

Market Outlook

Looking ahead, growth in the automatic reversing mill market will remain steady, with value increasingly concentrated among suppliers that integrate mechanical engineering with advanced automation and digital services. Steel producers seeking resilient, flexible, and energy-efficient rolling solutions will continue to favor automation-led investments.