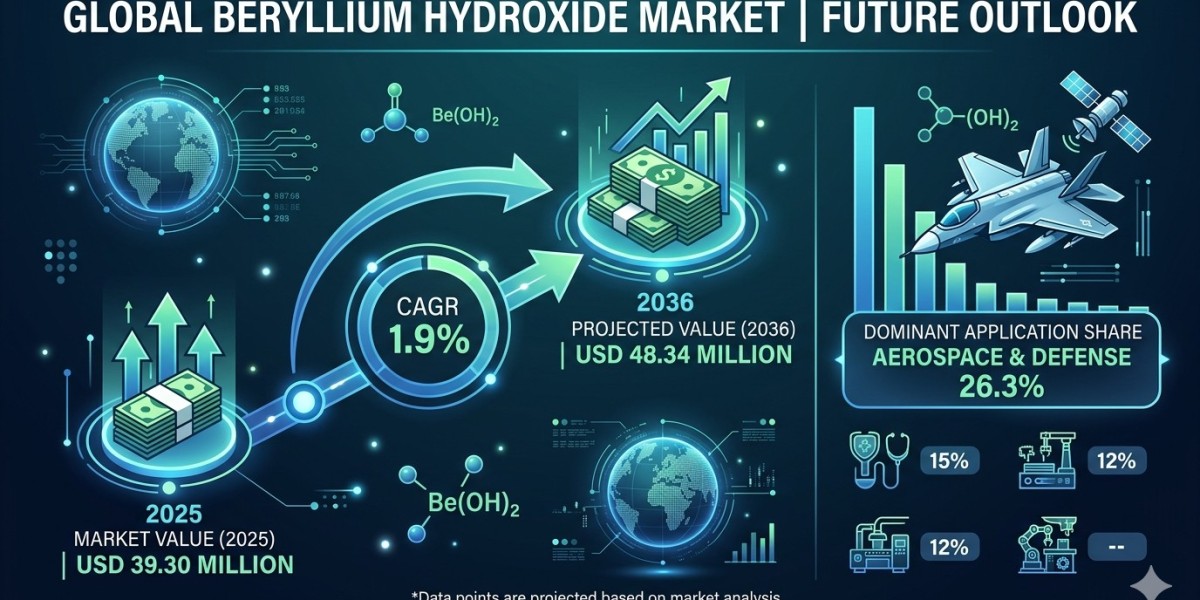

The global beryllium hydroxide market is projected to witness steady expansion over the next decade, supported by tightening technical requirements in critical engineering domains and rising industrial integration across high-performance sectors. The market is expected to grow steadily, reaching approximately USD 48.34 million by 2036, registering a CAGR of 1.9%, according to the latest analysis by Future Market Insights (FMI).

Market growth is being shaped by increasing demand in aerospace engineering, growing industrial utilization in advanced substrates, and specialized requirements within defense electronics. Beryllium hydroxide has evolved from a niche chemical intermediary into an essential material precursor across advanced civil and defense applications. While traditional aerospace uses continue to dominate consumption profiles, processing facilities are increasingly capitalizing on downstream innovations such as high-temperature electronics, sensors, and telecommunications hardware to satisfy evolving structural requirements and improve performance resilience under extreme operating conditions.

Beryllium Hydroxide Market Snapshot (2026–2036)

Market size outlook toward 2026: USD 40.05 million

Forecast value by 2036: USD 48.34 million

Forecast CAGR: 1.9% (2026 to 2036)

Dominant application category: Aerospace (26.3% market share in 2026)

Fastest-growing country segment: China (2.6% CAGR)

Primary demand channel: Defense, aerospace, and high-tech manufacturing OEM integration

Momentum in the Market

Beginning from steady baseline adoption levels, the global beryllium hydroxide market demonstrates continuous growth throughout the forecast period as technological dependencies solidify across critical industries. Between 2026 and 2036, expanding commercial space programs and rising defense sector modernizations are expected to significantly boost demand for refined intermediate materials. Increasing global communication infrastructure and higher computing density are encouraging component fabricators and material engineering firms to prioritize specialized thermal management and structural alloys.

From 2036 onward, innovation in extreme-environment ceramic components and deep integration with next-generation telecommunication grids is expected to further strengthen market expansion. Smart processing methods capable of optimizing extraction purity and enhancing output properties for specialized downstream manufacturing are emerging as key differentiators for primary refiners.

The Reasons Behind the Market’s Growth

Demand for beryllium hydroxide is rising due to multiple structural and technological factors reshaping the advanced materials and metallurgical ecosystem.

Rigid Aerospace and Defense Technical Demands

Defense organizations and aerospace firms worldwide are enforcing strict performance compliance requirements, demanding low weight, high thermal stability, and intense rigidity. Beryllium hydroxide serves as a non-negotiable intermediate precursor in producing high-performance alloys and structural components for these programs.

Expanding Semiconductor and Substrate Integration

Rapid expansion of advanced telecommunication hubs and data processing facilities is driving large-scale OEM adoption of ceramic and composite substrates that rely on beryllium compounds for efficient thermal management.

Growing Electronics Performance Criteria

Component fabricators are prioritizing materials that maintain strict dimensional tolerances under extreme physical duress, accelerating adoption across high-reliability sensor segments.

Emerging Strategic Stockpiling Programs

The rise of defense-focused material security initiatives is creating steady, contractual procurement cycles tailored to long-term national security reserves and highly specialized production line rollouts.

Top Segment Application Type

Aerospace Components Lead Market Demand

Aerospace architectures account for the majority of beryllium hydroxide material distribution channels globally, supported by increasing commercial flight deployment and strict defense program mandates requiring durable structural frameworks.

Application Dynamic Analysis

Aerospace: 26.3% dominant revenue share in 2026, driven by high-strength alloy and ceramic composite manufacturing.

Automotive Sensors: Steady deployment tied to high-temperature engine management and specialized telemetry.

Defense Electronics: High-purity tracking with rising electronic warfare and missile defense substrate integration.

Telecommunications Infrastructure: Durable material applications targeting long-term subsea and satellite connectivity platforms.

Regional Development: International Supply Chains and Manufacturing Hubs Drive Expansion

The global market is characterized by focused regional manufacturing ecosystems supported by advanced extraction centers and specialized downline alloy production facilities.

United States: A primary powerhouse in market consumption, estimated at USD 13.4 million in 2026 and projected to reach USD 15.8 million by 2036, advancing at a 1.6% CAGR due to deep-rooted aerospace and defense structures.

Germany: Leading Western European growth with a 2.2% CAGR, anchored by robust high-end automotive supply networks and precision machinery assembly.

China: Exploding as the fastest-growing regional segment at a 2.6% CAGR, propelled by rapid telecommunications scaling and industrial electronics demand.

India: Emerging strongly at a 2.4% CAGR, supported by modern industrial manufacturing investments and domestic aerospace defense initiatives.

Japan & South Korea: Positioned as highly technical demand centers valued at USD 1.8 million and USD 1.3 million respectively in 2026, driven by cutting-edge consumer electronics and advanced sensor component fabrication.

Challenges, Trends, Opportunities, and Drivers

Drivers

Mandatory structural performance specifications in aerospace

Rising defense budgets and electronics modernization programs

Increasing deployment of high-frequency communication networks

Expansion of space exploration and satellite constellation manufacturing

Opportunities

High-purity grades for advanced semiconductor test equipment

Biomedical applications and non-magnetic imaging component systems

Lightweight, resilient structural matrices for unmanned aerial systems (UAS)

Integration with advanced high-temperature ceramic architectures

Trends

Transition toward highly automated, clean refining processes

Increased adoption of multi-material metal matrix composites

Shift toward closed-loop material recycling within closed defense circles

Sustainability-focused regulatory compliance regarding handling safety

Challenges

High environmental and occupational safety handling stringency

Complex processing requirements and specialized facility costs

Concentrated and heavily controlled global supply chains

Country Growth Outlook (Global Economies)

The market’s growth trajectory is closely tied to defense industrialization and industrial policy implementation across primary nations:

United States: Strategic defense reserve procurement and commercial space industry leadership.

Germany: Premium automotive sensor integration and aerospace component export scaling.

China: Massive industrial electronics consumption and raw processing capacity expansions.

India: Modernizing aerospace infrastructure and domestic engineering capability shifts.

Japan: Precision engineering dominance and high-reliability component assembly needs.

The Competitive Environment

The global beryllium hydroxide market is highly consolidated, with a small number of Tier-1 chemical refiners and metallurgical companies controlling primary conversion capacity. Competitors focus on supply contract security, regulatory compliance engineering, and custom output optimization.

Leading international entities navigate this space by investing in workplace safety automation, sustainable purification methods, and integrated downstream conversion capabilities. Strategic partnerships with defense contractors and aerospace conglomerates remain central to maintaining supply chain position and protecting multi-year delivery pipelines.

Future Outlook: Toward Specialized and Resilient Technologies

The beryllium hydroxide market is entering a highly technical decade shaped by deep communication scaling, aerospace structural advancements, and rigid material sovereignty expectations. Future intermediate supply networks are expected to function alongside defense self-reliance strategies and high-reliability computing requirements. As target industries advance and component specifications narrow, beryllium hydroxide will remain foundational to building durable hardware solutions across critical global applications.

For a comprehensive strategic outlook and detailed analysis of technological developments shaping the industry, readers can explore the full report on the official Future Market Insights website: https://www.futuremarketinsights.com/reports/beryllium-hydroxide-market