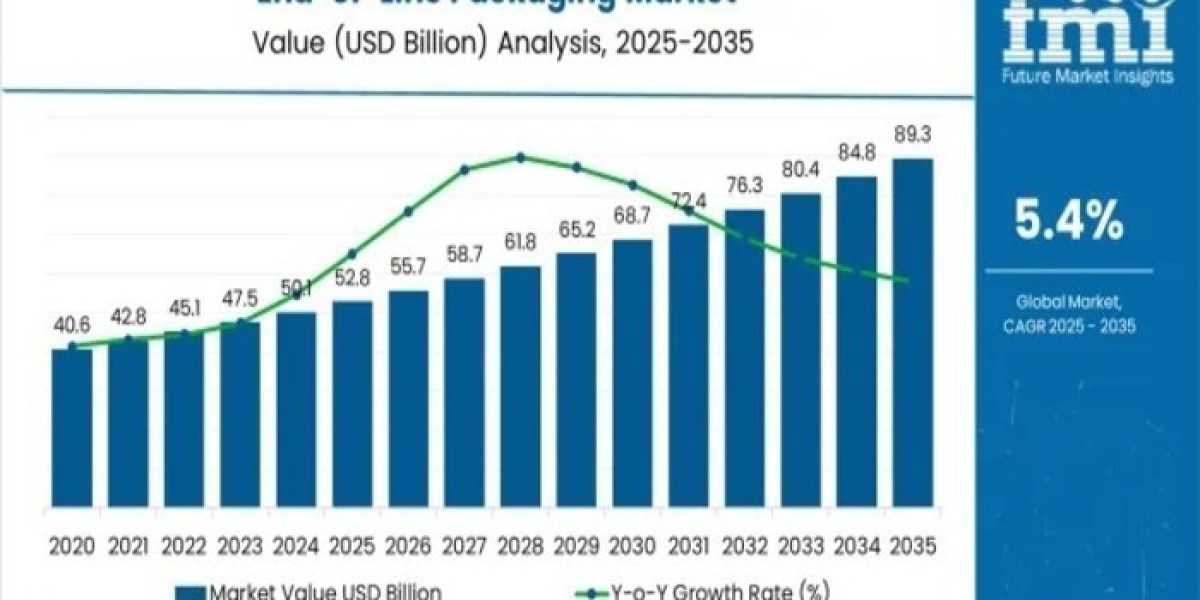

The global End-of-Line Packaging Market is entering a decade of accelerated transformation, fueled by automation, e-commerce growth, and digital integration across manufacturing operations. Valued at USD 52.8 billion in 2025, the market is forecast to reach USD 89.3 billion by 2035, expanding at a CAGR of 5.4%. According to the latest FMI analysis, this reflects a total increase of USD 36.6 billion a growth of 69.3% over the decade, with the overall market expected to scale 1.69X amid expanding industrial automation and smart packaging integration.

A Decade of Automation-Driven Transformation

Between 2025 and 2030, the market will rise from USD 52.8 billion to USD 69.7 billion, accounting for nearly 46% of total growth projected for the decade. This initial growth phase will be driven by expanding adoption of automated palletizing systems, robotic case packers, and high-speed wrapping machines particularly in food, beverage, and logistics sectors that demand efficiency and precision.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates – https://www.futuremarketinsights.com/reports/sample/rep-gb-15438

The subsequent 2030–2035 phase will witness another USD 19.7 billion expansion, supported by AI-enabled quality inspection systems, collaborative robotics, and smart vision sensors that redefine packaging precision and traceability. Manufacturers are rapidly embracing Industry 4.0 standards, prioritizing equipment connectivity, real-time analytics, and predictive maintenance as integral components of end-of-line (EOL) packaging architecture.

Regional Growth Momentum

The global landscape reveals striking regional dynamics.

- Asia Pacific leads with accelerated automation in India (8.6% CAGR) and China (7.3%), where manufacturing expansion, food processing, and e-commerce logistics are fueling rapid adoption.

- North America, led by the USA (4.8% CAGR), emphasizes pharmaceutical serialization, flexible automation, and robotic packaging integration.

- Europe continues to leverage its precision engineering capabilities, with Germany (4.5% CAGR) at the forefront of high-speed automation in pharmaceuticals and food sectors.

- Brazil (6.2%) and Mexico (5.9%) demonstrate strong growth in beverage packaging and nearshoring-driven manufacturing, respectively.

Food & Beverage and Pharmaceuticals Remain the Core Pillars

The food & beverage sector, commanding 42.8% of market demand, continues to dominate EOL packaging investments, driven by rising production volumes and quality standardization. Meanwhile, the pharmaceutical industry is rapidly emerging as the fastest-growing segment, adopting serialization, track-and-trace, and tamper-evident systems to meet stringent global compliance requirements.

EOL packaging is no longer viewed as a terminal process but as a strategic enabler of production efficiency, supply chain reliability, and regulatory compliance—particularly as manufacturers pursue leaner, smarter, and more sustainable operations.

Key Opportunity Pathways

FMI identifies seven opportunity clusters that will shape market competitiveness through 2035:

- Robotic Palletizing & Case Packing Systems (USD 8.9–12.6 Bn) – Multi-axis robotic palletizers with adaptive learning capabilities are emerging as high-margin technologies for high-volume operations.

- Integrated IoT-Connected Packaging Lines (USD 6.8–9.7 Bn) – Demand for real-time performance monitoring and predictive maintenance is fueling adoption of IoT-enabled systems.

- High-Speed Wrapping & Stretch Film Systems (USD 5.4–7.8 Bn) – Efficiency-driven logistics and sustainability-focused film consumption drive growth in pre-stretch wrapping.

- Pharmaceutical Serialization & Track-and-Trace (USD 4.9–7.1 Bn) – Compliance-focused automation presents strong opportunities in pharma manufacturing hubs.

- Localized Service Networks (USD 7.6–11.2 Bn) – In Asia and Latin America, manufacturers with on-ground service support enjoy faster commissioning and uptime advantages.

- Compact & Modular Systems (USD 3.8–5.6 Bn) – Scalable, space-efficient systems cater to SMEs and craft manufacturers.

- Vision Inspection Integration (USD 4.2–6.3 Bn) – Automated defect detection and label verification ensure packaging integrity across regulated industries.

Palletizers Lead Equipment Adoption

By equipment type, palletizers account for 36.2% of total installations in 2025, underpinning their foundational role in material handling and load formation. These systems remain essential for throughput optimization in food, beverage, and consumer goods production lines.

Similarly, primary packaging completion representing 28.5% of total applications, reflects manufacturers’ growing need for accurate filling, sealing, and labeling operations that maintain product integrity and brand presentation.

Market Dynamics: Drivers and Challenges

The global end-of-line packaging market benefits from structural trends:

- Automation as a necessity: Labor shortages and rising wages are pushing manufacturers toward unmanned packaging solutions.

- Operational efficiency: EOL systems improve consistency, reduce downtime, and enhance throughput rates.

- Digital integration: IoT and AI technologies enable predictive maintenance and real-time performance insights.

However, high capital investment costs and integration complexities remain adoption barriers, particularly for small and mid-sized producers. Equipment suppliers are addressing this gap with modular architectures and subscription-based automation models.

Competitive Landscape

The market’s competitive intensity is shaped by a mix of global leaders and specialized automation firms:

Krones AG, Sidel Group, IMA Group, Barry-Wehmiller Companies, Bosch Packaging Technology, and Wirtgen Group dominate with extensive automation portfolios, while regional players like Combi Packaging Systems, Columbia Machine, and Premier Tech Chronos strengthen localized service networks.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.