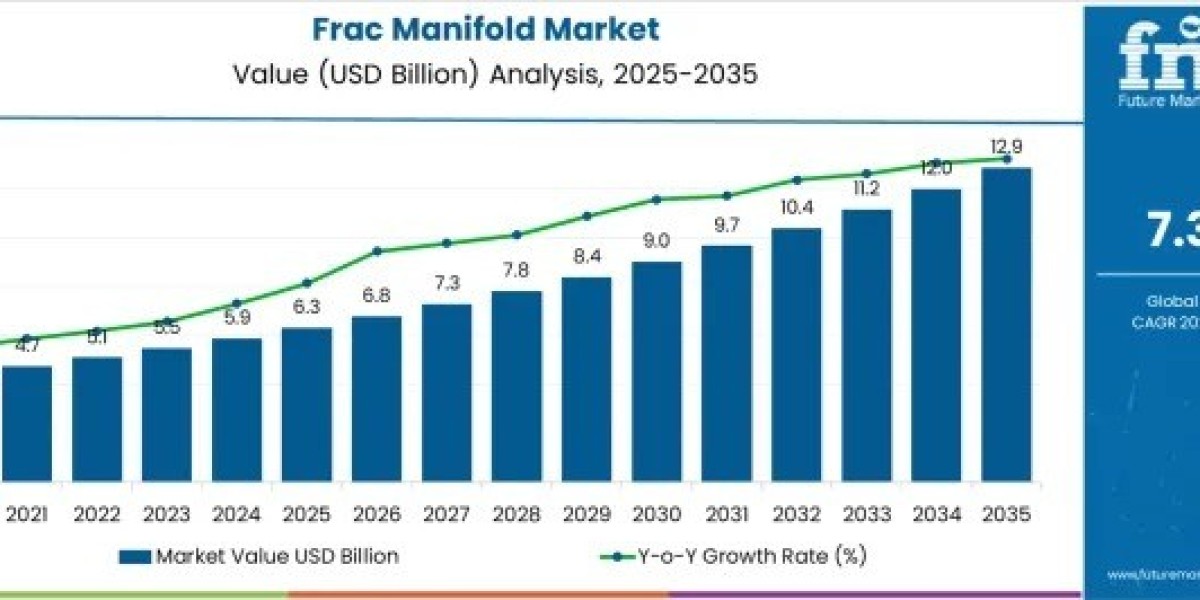

The Frac Manifold Market is entering a decade of sustained expansion, supported by rising unconventional oil and gas activity and the industry’s focus on operational reliability. Valued at USD 6.3 billion in 2025, the market is projected to reach USD 12.9 billion by 2035, registering a CAGR of 7.3% over the forecast period. This growth reflects the essential role of frac manifolds in managing high-pressure fluid flow during complex, multi-stage hydraulic fracturing operations.

As shale development intensifies across North America, Asia-Pacific, and parts of Europe, operators are increasingly investing in advanced pressure control equipment to reduce downtime, improve safety, and optimize well completion efficiency. Frac manifolds, once viewed as auxiliary equipment, are now recognized as core infrastructure in modern fracturing spreads.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates:

https://www.futuremarketinsights.com/reports/sample/rep-gb-19576

Market Fundamentals: Efficiency, Safety, and Scale

The steady rise of the frac manifold market is closely linked to the global push for cost-efficient hydrocarbon extraction. As wells become deeper and fracturing stages multiply, the need for reliable systems capable of handling extreme pressures has intensified. Industry updates highlight that operators are prioritizing manifolds that support faster rig-up and rig-down times, minimize leak risks, and integrate seamlessly with high-capacity pumping units.

Key market highlights include:

- Growing demand from unconventional oil and gas fields

- Increased focus on reducing non-productive time (NPT)

- Investments by oilfield service providers in modular and scalable manifold systems

- Rising adoption of automation and digital monitoring technologies

Horizontal Frac Manifolds Lead Integration Preferences

Horizontal frac manifolds are projected to account for 52.3% of market revenue in 2025, making them the leading integration type. Their dominance is rooted in operational simplicity and enhanced safety. Horizontal designs streamline fluid alignment, reduce equipment footprint, and lower the risk of worker exposure during high-pressure operations.

Manufacturers and field operators report that horizontal manifolds offer consistent flow control while reducing wear and tear, ultimately extending service life. Their modular nature also supports integration with digital monitoring systems, making them well-suited for large-scale shale and pad drilling projects.

Carbon Steel Remains the Material of Choice

From a material standpoint, carbon steel manifolds are expected to hold 57.8% of market revenue in 2025. The segment’s leadership is driven by its proven performance under extreme pressure and abrasive conditions. Carbon steel offers an optimal balance of strength, durability, availability, and cost-effectiveness—critical factors for operators managing large fracturing fleets.

While advanced alloys and composites continue to gain attention, industry consensus indicates that carbon steel will remain the preferred option for most applications due to its reliability and established manufacturing ecosystem.

Multiple Outlet Configurations Drive Operational Flexibility

Multiple outlet frac manifolds are forecast to contribute 62.1% of market revenue in 2025, reflecting their importance in multi-well, multi-stage fracturing operations. These systems enable simultaneous fluid distribution across several wellheads, reducing pumping interruptions and improving overall fracturing efficiency.

As pad drilling becomes standard practice, multiple outlet configurations are increasingly viewed as essential for maximizing asset utilization and minimizing operational delays. Their scalability aligns well with the industry’s push toward higher productivity per well pad.

Regional Growth Dynamics Shape Market Opportunities

North America continues to anchor global demand, supported by technological leadership and extensive shale reserves. Asia-Pacific, led by China and India, is emerging as a high-growth region as governments invest in domestic energy security and unconventional resource development. Europe and Japan are also contributing through targeted investments in advanced oilfield technologies and overseas energy projects.

Country-level trends indicate moderate to strong growth across the United States, China, India, Japan, and the United Kingdom, with government policies, infrastructure spending, and technological innovation acting as key catalysts.

Competitive Landscape and Strategic Developments

The frac manifold market is characterized by the presence of global oilfield service leaders and specialized equipment manufacturers, including SLB, Jereh Group, NOV, Weatherford International, Halliburton, and Worldwide Oilfield Machine (WOM). Competitive strategies increasingly focus on product innovation, partnerships, and expansion into emerging markets.

Recent developments underscore this trend. In May 2025, Jereh Group launched advanced fracturing solutions and new plunger pump systems, strengthening its competitive position. In April 2025, SLB introduced next-generation artificial lift systems designed to enhance performance across complex operations.

Looking Ahead: Digitalization and Predictive Maintenance

Future growth of the frac manifold market will be shaped by digital transformation. Integration of IoT sensors, AI-driven analytics, and predictive maintenance tools is expected to improve reliability, enhance safety, and reduce lifecycle costs. As energy demand rises with urbanization and population growth, frac manifolds will remain indispensable to efficient hydrocarbon production.

terly and annual data updates:

https://www.futuremarketinsights.com/reports/sample/rep-gb-18825

Market Momentum Shaped by Regulation and Industrial Expansion

Global enforcement of occupational safety standards continues to be the strongest growth catalyst. Regulatory bodies across North America, Europe, and Asia-Pacific are tightening compliance requirements, pushing companies to adopt certified fall arrest, restraint, and positioning systems. These regulations are reinforced by rising insurance scrutiny and the financial implications of workplace accidents, including penalties, downtime, and reputational damage.

At the same time, large-scale infrastructure development, urbanization, and industrial expansion—particularly in emerging economies—are creating sustained demand for fall protection solutions. High-rise residential and commercial construction, renewable energy installations, and maintenance of aging industrial assets are all height-driven activities that require robust fall protection frameworks.

Soft Goods Dominate Product Demand

By product type, soft goods lead the market with a commanding 58.3% share in 2025. This segment includes harnesses, lanyards, and lifelines that form the backbone of personal fall arrest systems. Their dominance is driven by several factors:

- Lightweight and ergonomic designs that improve worker comfort and compliance

- Advancements in high-strength fibers and impact-resistant webbing

- Cost-effectiveness and adaptability across multiple industries

Continuous innovation in materials science has enhanced durability without compromising flexibility, making soft goods the preferred choice across construction, oil and gas, utilities, and telecommunications. With a projected CAGR of 6.9% through 2035, soft goods are expected to maintain their leadership position.

Construction Remains the Largest End-Use Segment

The construction industry accounts for approximately 35.7% of total fall protection demand, reflecting the inherently high-risk nature of working at heights. From scaffolding and roofing to bridges and large infrastructure projects, construction sites rely heavily on fall protection equipment to meet safety mandates and reduce accident rates.

Key factors supporting growth in this segment include:

- Stringent national and regional safety regulations

- Rapid urbanization and infrastructure investment in Asia-Pacific and the Middle East

- Growing availability of rental and modular fall protection systems

With construction activity projected to remain strong globally, this segment is forecast to grow at a CAGR of 6.7% through 2035.

Regional Outlook: Safety Standards Drive Adoption

North America, Europe, and Asia-Pacific collectively represent the most significant growth regions. The United States market continues to expand at a CAGR of 7.2%, supported by strict OSHA regulations and rising investment in worker insurance and risk mitigation. Employers increasingly view fall protection as a means to reduce long-term liability and improve workforce retention.

Japan stands out with an estimated CAGR of 8.5% by 2035, reflecting its strong commitment to precision, technological integration, and workplace safety in construction and manufacturing. Similarly, the United Kingdom (8.3%) and South Korea (8.2%) demonstrate proactive adoption driven by regulatory enforcement and industrial modernization. China’s 7.4% growth rate underscores the scale of its construction and industrial workforce and the need for standardized safety systems.

Technology and Smart Safety Systems Reshape the Market

Innovation is redefining the competitive landscape. Manufacturers are increasingly integrating IoT-enabled sensors into harnesses and lifelines, enabling real-time monitoring, incident alerts, and predictive safety analytics. These smart systems help employers move from reactive accident prevention to proactive risk management.

Ergonomic design improvements and customization for industry-specific applications are also gaining traction. As a result, fall protection equipment is evolving from basic PPE into intelligent safety solutions aligned with digital workplace strategies.

Competitive Landscape and Strategic Developments

The fall protection market features established global players alongside innovative entrants, creating a dynamic and competitive environment. Companies such as 3M, Honeywell International, MSA Safety, Petzl, WernerCo., Guardian Fall, and SKYLOTEC continue to strengthen their portfolios through R&D, partnerships, and acquisitions.

Recent developments highlight this trend. In May 2024, MSA Safety acquired Bacharach Inc. to expand its gas detection and safety solutions portfolio. In December 2025, Guardian partnered with Twiceme Technology to integrate advanced smart safety features into its B7-Comfort Harness, signaling growing momentum toward connected PPE.