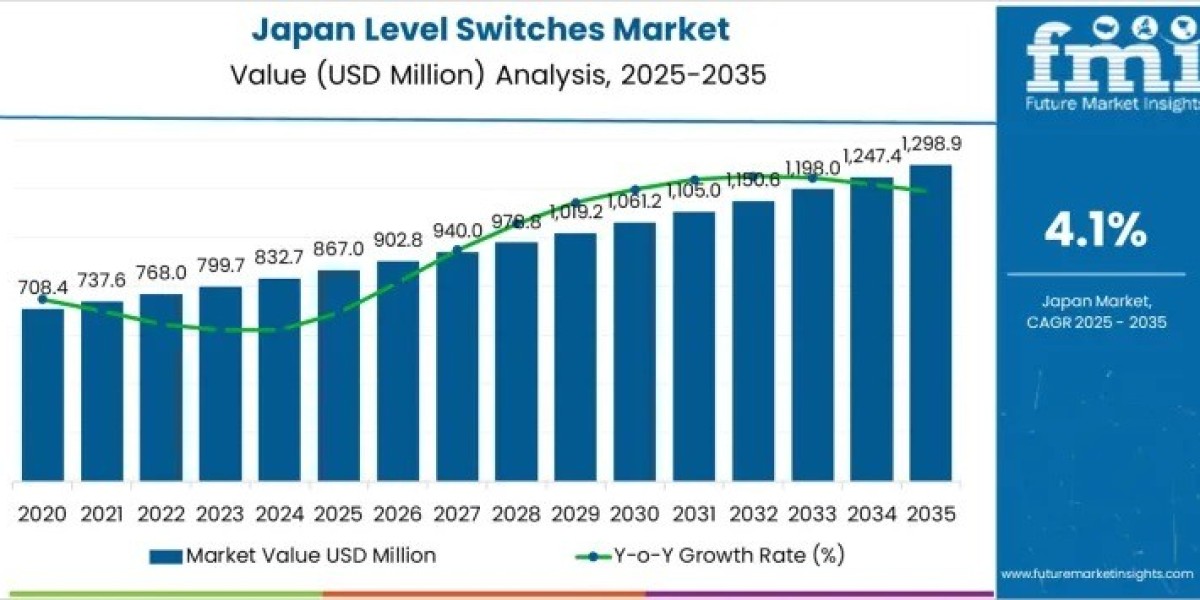

The Demand for Level Switches in Japan is poised for steady expansion, reaching USD 1,298.9 million by 2035 from USD 867.0 million in 2025, at a CAGR of 4.1%. This growth is fueled by industrial automation, compliance with safety regulations, and modernization of chemical, water treatment, food, and power generation facilities. Float level switches dominate the market due to their versatility in liquid holding tanks and general-purpose vessel monitoring. Capacitive and conductivity switches further enhance capabilities for closed vessel and reservoir applications where contact-based detection is critical.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates: https://www.futuremarketinsights.com/reports/sample/rep-gb-29761

Early demand was shaped by maintenance cycles, safety interlocks, and regulatory process control requirements rather than new plant construction. From 2026 onward, the market value is expected to rise steadily, supported by automation in grain silos, hoppers, and bulk material handling systems. Advanced technologies such as tuning fork and optical switches are increasingly adopted in dusty or abrasive environments where traditional float mechanisms are less reliable.

Key Market Drivers and Trends

- Industrial Process Automation: Automated level control ensures precision dosing, overflow prevention, and dry run protection across chemical, food, and water plants.

- Safety and Compliance: Earthquake-prone regions and strict safety standards necessitate reliable level detection to protect equipment and personnel.

- Replacement Demand: Post-2030 growth is largely driven by sensor upgrades and incremental density rather than new installations.

- Technological Advancements: Non-contact sensing, vibration-based designs, and digital output models are increasingly preferred in corrosive, high-temperature, or hygienic environments.

Switch Type and Application Insights

- Float Level Switches (40% share): Favored for mechanical simplicity, reliability, and low failure rates in chemical processing, food manufacturing, water treatment, and boiler systems. Standardization and repeat maintenance cycles support predictable procurement patterns.

- Liquid Holding Tanks (44% share): Represent the primary application due to their central role in storage, batching, and treatment operations. Operators prioritize reliable overflow prevention and pump protection.

Daily usage across chemical, water, and food plants emphasizes operational safety and process repeatability. For power generation, wastewater, and bulk handling, the demand for robust, vibration-resistant, and fail-safe devices is rising, reflecting tighter process safety regulations and lifecycle reliability expectations.

Regional Adoption Patterns

- Kyushu & Okinawa: Leading the market with a 5.2% CAGR, driven by chemical processing, water treatment, food manufacturing, and port-based fuel storage.

- Kanto: Growing at 4.7% CAGR, fueled by pharmaceutical, electronics, and wastewater management operations.

- Kansai: Moderate 4.2% CAGR, supported by machinery manufacturing, beverage production, and petrochemical handling.

- Chubu: 3.7% CAGR, driven by automotive, metalworking, and hydraulic systems.

- Tohoku & Rest of Japan: 3.2% and 3.1% CAGR, reflecting smaller industrial density but steady replacement demand.

Key Players Driving Market Expansion

- Dwyer Instruments – Mechanical and digital switches for HVAC and industrial tanks.

- AMETEK Inc. – Precision sensing platforms for laboratory and industrial applications.

- SICK AG – Non-contact and optical level detection for materials handling and packaging automation.

- Gems Sensors & Controls – Compact level switches for hydraulic systems and small vessels.

- FineTek Co. Ltd. – Capacitive and vibration-based switches for food, plastics, and bulk processing.

These suppliers emphasize reliability, corrosion resistance, Japanese-language support, and rapid maintenance response, shaping procurement across core industrial regions.

Strategic Market Outlook

Looking ahead, Japan’s level switch demand will be driven by deeper automation, digital integration, and infrastructure renewal. Investment decisions reflect plant reinvestment cycles, compliance requirements, and the need for predictive maintenance. As manufacturing plants and utility facilities modernize, the market will benefit from higher sensor density, real-time monitoring, and system-wide diagnostics capabilities.