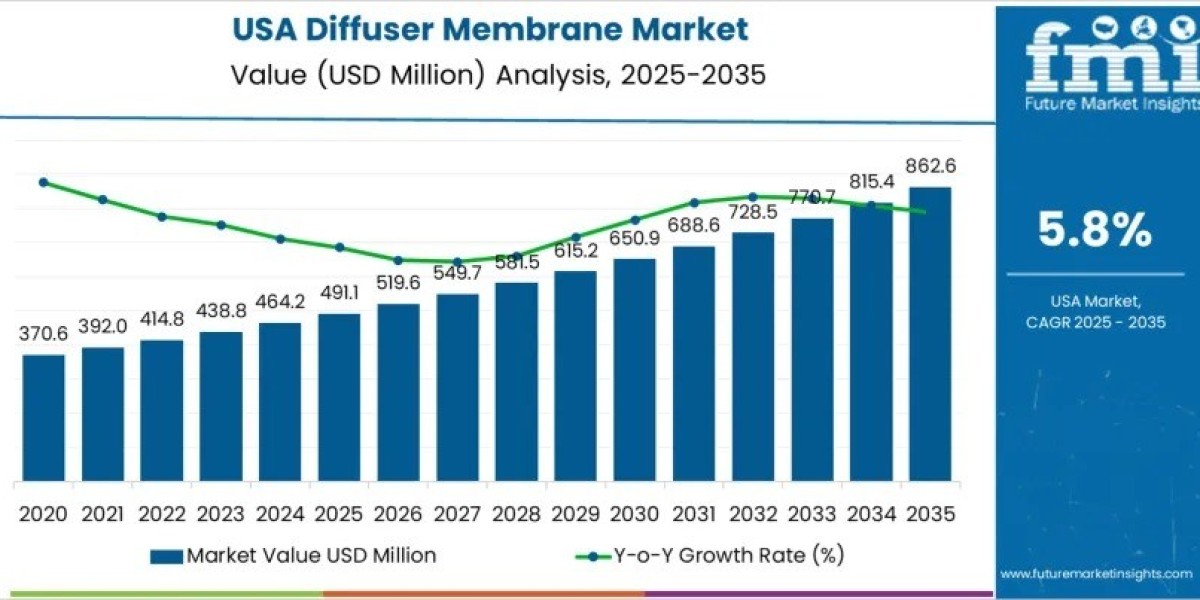

The Demand for Diffuser Membrane in USA is gaining momentum as wastewater treatment operators prioritize energy efficiency and regulatory compliance. Valued at USD 491.1 million in 2025, the market is projected to reach USD 862.6 million by 2035, registering a CAGR of 5.8%. Growth is anchored in the modernization of municipal wastewater treatment plants and increased adoption of fine-bubble aeration systems that lower power consumption while improving oxygen-transfer efficiency.

Rising expectations for effluent quality across federal and state jurisdictions are accelerating replacement of aging coarse-bubble aeration systems. Diffuser membranes enable consistent oxygen delivery with reduced blower energy, making them a preferred solution for utilities seeking long-term operational savings alongside compliance.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-29505

Key Data Points:

- Market value grows from USD 491.1 million (2025) to USD 862.6 million (2035)

- Forecast CAGR (2025–2035): 5.8%

- Growth driven by infrastructure upgrades and energy optimization

Infrastructure Modernization and Regulation Fuel Demand

Municipal wastewater treatment plants represent the backbone of USA diffuser membrane demand. Many facilities operate decades-old infrastructure that struggles to meet modern discharge standards for biological oxygen demand (BOD), nitrogen, and nutrient removal. Capital improvement programs across major states are prioritizing aeration upgrades as a cost-effective path to compliance.

Industrial wastewater treatment also contributes to sustained demand. Food processing, chemical manufacturing, and pharmaceutical facilities increasingly install diffuser membranes to stabilize biological treatment processes before discharge or reuse. These investments support predictable procurement cycles and reinforce the market’s steady growth curve.

Key Drivers:

- Regulatory pressure on effluent quality

- Aging wastewater infrastructure requiring upgrades

- Focus on reducing energy intensity in aeration processes

EPDM Emerges as the Preferred Material

Material performance remains central to purchasing decisions. EPDM membranes dominate USA demand due to their mechanical strength, chemical resistance, and durability under continuous operation. Their ability to maintain elasticity over long cycles helps limit maintenance frequency, supporting cost-control objectives in large-scale installations.

Polyurethane membranes are selected for industrial environments requiring higher abrasion resistance, while silicone membranes serve niche applications needing thermal stability and reduced fouling. Overall, material choices reflect a lifecycle-cost perspective rather than upfront pricing alone.

Material Insights:

- EPDM leads adoption due to durability and cost efficiency

- Polyurethane supports demanding industrial conditions

- Silicone remains niche but relevant for specialty use cases

Flow Capacity and End-User Adoption Patterns

High-capacity diffuser membranes account for the largest share of demand, supporting major municipal wastewater plants where aeration efficiency directly impacts operating budgets. These systems reduce blower load requirements and deliver consistent oxygen transfer in large basins.

Low-capacity membranes are increasingly used in decentralized treatment systems, small municipalities, and aquaculture operations. Medium-capacity solutions serve balancing tanks and compact industrial vessels, reflecting the diversity of USA treatment infrastructure.

End-User Breakdown:

- Municipal wastewater treatment leads adoption

- Industrial wastewater treatment supports steady demand

- Aquaculture and fish farming add incremental growth

Regional Demand Trends Across the United States

Regional growth mirrors infrastructure investment intensity and regulatory enforcement. West USA leads with the fastest growth, driven by sustainability initiatives and large-scale treatment upgrades in states such as California and Washington. Utilities in this region prioritize membranes that deliver higher oxygen-transfer efficiency and lower long-term energy costs.

The South USA follows, supported by industrial wastewater requirements and rapid urban population growth. Northeast USA demand is shaped by strict environmental regulations and aging infrastructure replacement, while Midwest USA growth reflects municipal rehabilitation programs and food-processing wastewater needs.

Regional Highlights:

- West USA: Fastest growth driven by sustainability upgrades

- South USA: Industrial effluent and urban expansion

- Northeast USA: Compliance-led infrastructure replacement

- Midwest USA: Municipal rehabilitation and manufacturing activity

Competitive Landscape Focused on Performance and Reliability

Competition in the USA diffuser membrane market centers on lifecycle performance, fouling resistance, and service support. Key suppliers include Pentair (AquaVation), Aquasource, SSI, Koch Membrane Systems, and Xylem (Sanitaire). Their strategies emphasize longer service life, enhanced diffuser configurations, and reliable spare-part availability to minimize downtime during maintenance cycles.

Utilities increasingly favor suppliers that provide documented efficiency gains and strong after-sales support, reinforcing the importance of performance validation in procurement decisions.

Competitive Priorities:

- Extended membrane lifespan

- Resistance to fouling and chemical exposure

- Reliable service and replacement support

Market Outlook Through 2035

Looking ahead, USA diffuser membrane demand will remain closely tied to regulatory modernization and energy-efficiency goals. Integration with dissolved-oxygen sensors and automated control systems will further optimize aeration performance. Growth will increasingly depend on replacement cycles, decentralized treatment adoption, and niche applications such as aquaculture.

As utilities and industries align infrastructure spending with sustainability and cost-efficiency objectives, diffuser membranes are set to remain a core component of USA wastewater treatment strategies through 2035.