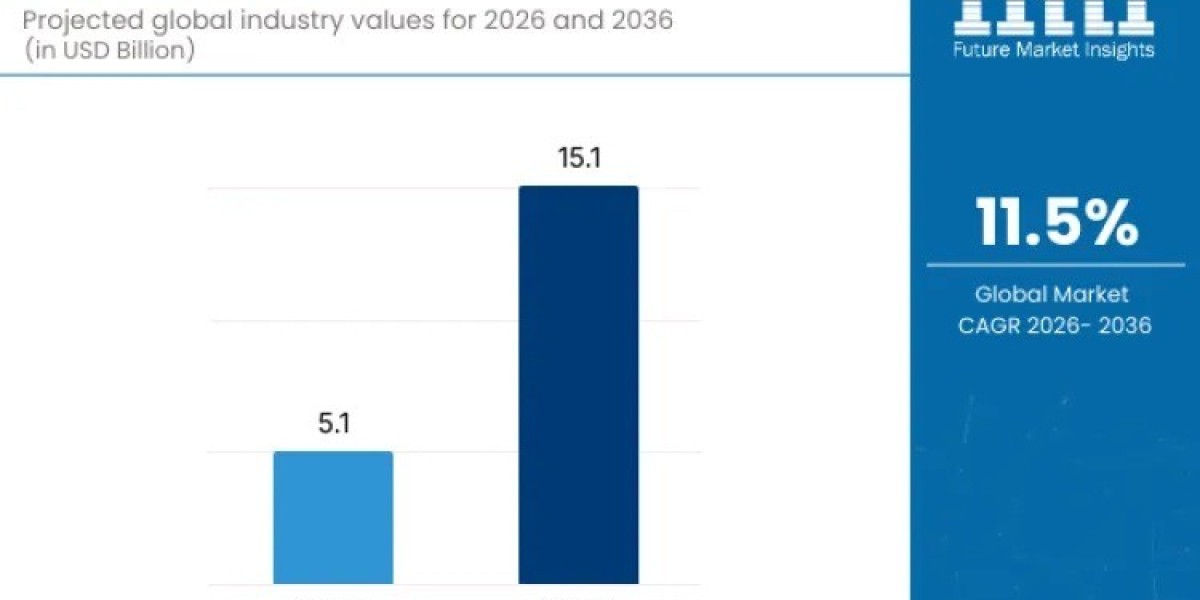

The global Fiber Laser Market is witnessing sustained growth as manufacturers prioritize precision, speed, and automation across production environments. Valued at USD 5.1 billion in 2026, the market is forecast to reach USD 15.1 billion by 2036, registering a CAGR of 11.5%. This expansion is closely tied to rising demand for advanced laser technologies that enhance cutting accuracy, reduce operational downtime, and improve production consistency across industrial sectors.

Fiber lasers are increasingly preferred over conventional laser systems due to their superior beam quality, high energy efficiency, compact design, and longer operational life. These advantages are reinforcing their adoption across metal processing, automotive manufacturing, electronics fabrication, and heavy industrial applications.

Automation and Smart Manufacturing Driving Adoption

Manufacturing automation is a primary catalyst shaping fiber laser demand. As factories integrate robotics, digital controls, and real-time monitoring systems, fiber lasers fit seamlessly into automated production lines. Their ability to deliver stable, repeatable performance supports manufacturers’ goals of reducing material waste, increasing throughput, and meeting stringent quality benchmarks.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates:

https://www.futuremarketinsights.com/reports/sample/rep-gb-8174

Key automation-driven factors include:

- Integration with advanced control and monitoring systems

- Improved cutting precision across high-volume production

- Reduced maintenance and downtime compared to traditional lasers

CW Lasers Lead by Technology Type

Continuous Wave (CW) fiber lasers dominate global demand, accounting for 76.1% of the market. Their leadership is driven by consistent power delivery, superior beam stability, and high efficiency in continuous industrial operations. CW lasers are widely deployed in cutting and welding applications where uninterrupted performance is critical.

Supporting trends include:

- Reliable performance across diverse manufacturing workflows

- Compatibility with automated and high-speed production lines

- Lower operating costs over long production cycles

Pulsed and QCW lasers continue to serve niche and precision-focused applications, ensuring balanced adoption across specialized industrial requirements.

High-Power Output Systems Dominate Market Share

High-power fiber lasers represent the largest output power segment, holding 62.7% of global demand. These systems are essential for heavy-duty cutting, thick material processing, and high-speed industrial operations. Their adoption reflects growing complexity in manufacturing processes and the need for standardized performance in large-scale production facilities.

Key segment dynamics include:

- High-power systems enabling faster processing of thick materials

- Medium-power lasers balancing cost and performance in general manufacturing

- Low-power lasers supporting fine and microprocessing applications

Cutting Applications Anchor Market Demand

Cutting applications account for 44.2% of the fiber laser market, making them the leading application segment globally. Automated cutting lines, precision metal fabrication, and industrial material processing continue to drive strong demand.

Additional application insights:

- Welding and high-power applications support heavy manufacturing and structural assembly

- Marking applications address traceability and quality control needs

- Balanced demand across processing and assembly-driven industries

Asia-Pacific and North America Remain Key Growth Engines

Regional growth is strongest across East Asia, South Asia & Pacific, and North America. India leads with a projected CAGR of 16.8%, supported by expanding manufacturing infrastructure and government-backed industrial modernization initiatives. China follows with a 15.2% CAGR, driven by large-scale automation adoption and precision manufacturing expansion.

Other notable regional trends include:

- USA growing at 12.9% CAGR with strong demand from automotive and advanced manufacturing

- Germany expanding at 11.7% CAGR through precision engineering and industrial excellence programs

- Japan growing at 10.5% CAGR, driven by advanced technology integration and quality-focused manufacturing

Competitive Landscape Shaped by Innovation and Scale

The fiber laser market is highly competitive, with leading players focusing on innovation, scalability, and integration capabilities. IPG Photonics, TRUMPF, Coherent, FANUC, and Raycus are shaping market dynamics through advanced laser platforms, high-performance cutting systems, and automation-ready solutions.

Competitive strategies include:

- Continuous R&D to enhance beam quality and efficiency

- Scalable solutions for high-volume manufacturing

- Strategic partnerships with automation and system integrators

Strategic Outlook for the Fiber Laser Market

As manufacturers pursue digitalization and operational efficiency, fiber lasers are becoming foundational to modern production ecosystems. Their role in supporting smart factories, reducing processing costs, and delivering consistent quality positions them as a long-term growth technology across industries.