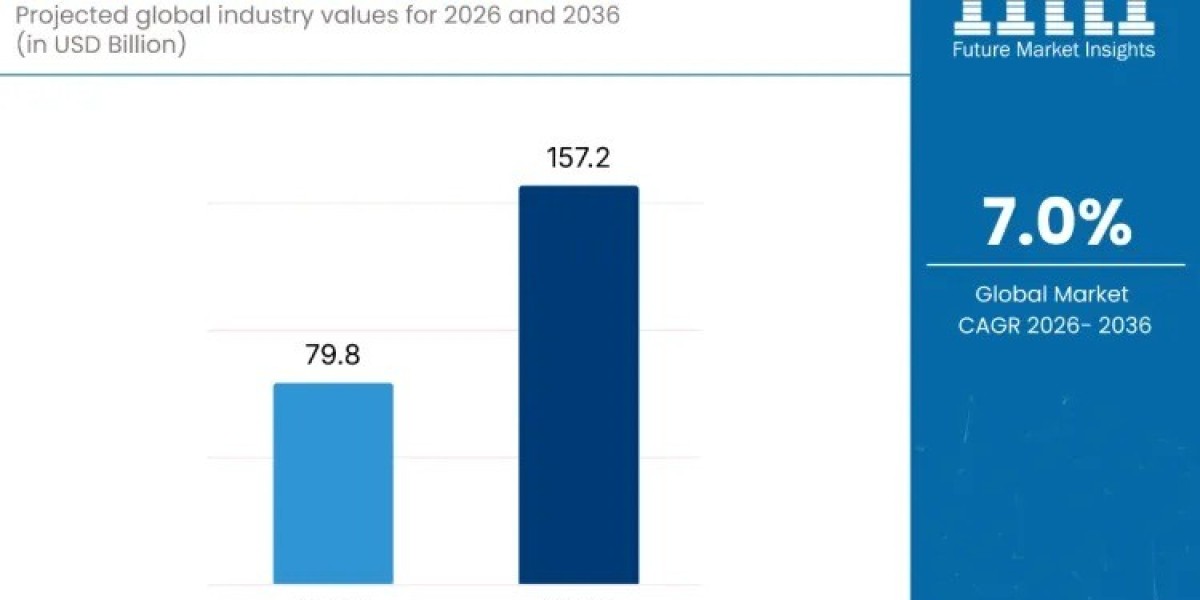

The global Water Treatment Market is entering a decisive growth phase, supported by urgent water security challenges and accelerating infrastructure investments. Valued at USD 79.8 billion in 2026, the market is forecast to nearly double, reaching USD 157.2 billion by 2036, expanding at a steady CAGR of 7.0%. This growth reflects mounting concerns around water scarcity, pollution, and regulatory compliance, alongside the growing need for safe, reliable water across municipalities and industries.

Governments and industries alike are prioritizing water treatment as a core component of sustainable development. Advanced technologies—including reverse osmosis (RO), membrane bioreactors (MBR), ultraviolet (UV) disinfection, and microfiltration—are increasingly deployed to ensure consistent water quality, resource efficiency, and regulatory adherence across diverse applications.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-5332

This subscription approach allows decision-makers to track regulatory shifts, technology adoption, and regional investment patterns as they unfold.

Key Growth Drivers Shaping the Market

Several structural forces are propelling the water treatment market forward:

- Rising water scarcity: Over two billion people live in water-stressed regions, intensifying demand for treatment, recycling, and reuse solutions.

- Urbanization and industrialization: Rapid population growth in emerging economies is straining existing water infrastructure.

- Regulatory pressure: Stricter discharge norms and drinking water standards are accelerating system upgrades.

- Technological progress: Innovations in membrane efficiency, AI-driven monitoring, and predictive maintenance are improving performance while lowering lifecycle costs.

Together, these factors are transforming water treatment from a compliance-driven necessity into a strategic enabler of industrial continuity and urban resilience.

Segment Insights: Where Demand Is Concentrated

Reverse osmosis systems account for the largest system-type share, representing roughly 29% of the market in 2026. Their ability to remove dissolved salts and complex contaminants makes RO indispensable for desalination, industrial process water, and municipal purification. Continuous improvements in membrane durability and energy efficiency are reinforcing RO’s dominance.

From an application perspective, wastewater treatment leads the market, holding about 36% share. Tightened environmental regulations and the global push toward water reuse have elevated wastewater treatment as a critical investment area. Municipalities and industries are increasingly adopting advanced filtration and purification technologies to recover resources and meet compliance standards.

Regional Outlook: Emerging Markets Take the Lead

While North America and Europe remain mature, high-value markets, the strongest growth momentum is shifting toward Asia. South Asia & Pacific and East Asia are emerging as pivotal regions due to rapid urbanization, industrial expansion, and government-backed water security initiatives.

- India is the fastest-growing market, with a projected CAGR of 11.6% through 2036. Large-scale infrastructure upgrades, urban demand, and water-intensive industries such as textiles and food processing are key drivers.

- China, growing at 7.5%, continues to invest heavily in industrial water recycling and zero liquid discharge systems under its environmental reform programs.

- The UK and USA are focused on modernizing aging infrastructure and integrating smart water management solutions, while

- Germany leverages advanced, chemical-free technologies to support industrial efficiency and EU compliance.

Competitive Landscape: Innovation as a Differentiator

The water treatment market is highly competitive, led by established global players such as Veolia Environnement, SUEZ, Xylem Inc., and Pentair. These companies are expanding their portfolios beyond equipment to include digital monitoring, lifecycle services, and performance optimization.

At the same time, challengers and regional specialists are gaining traction by offering tailored solutions for specific industries and local regulatory environments. In high-growth markets, localized expertise and customization capabilities are becoming decisive competitive advantages.

Challenges and Strategic Considerations

Despite strong growth prospects, high capital costs and system complexity remain notable barriers, particularly for smaller municipalities and enterprises. Skilled labor shortages and rising operational expenses also pose challenges. However, increasing adoption of modular systems, automation, and energy-efficient designs is helping to mitigate these constraints over time.

Looking Ahead: Water Treatment as a Strategic Asset

Over the next decade, water treatment will increasingly be viewed as a strategic asset rather than a cost center. Investments in reuse, recycling, and smart monitoring will define competitive advantage for industries and determine long-term water security for cities worldwide.