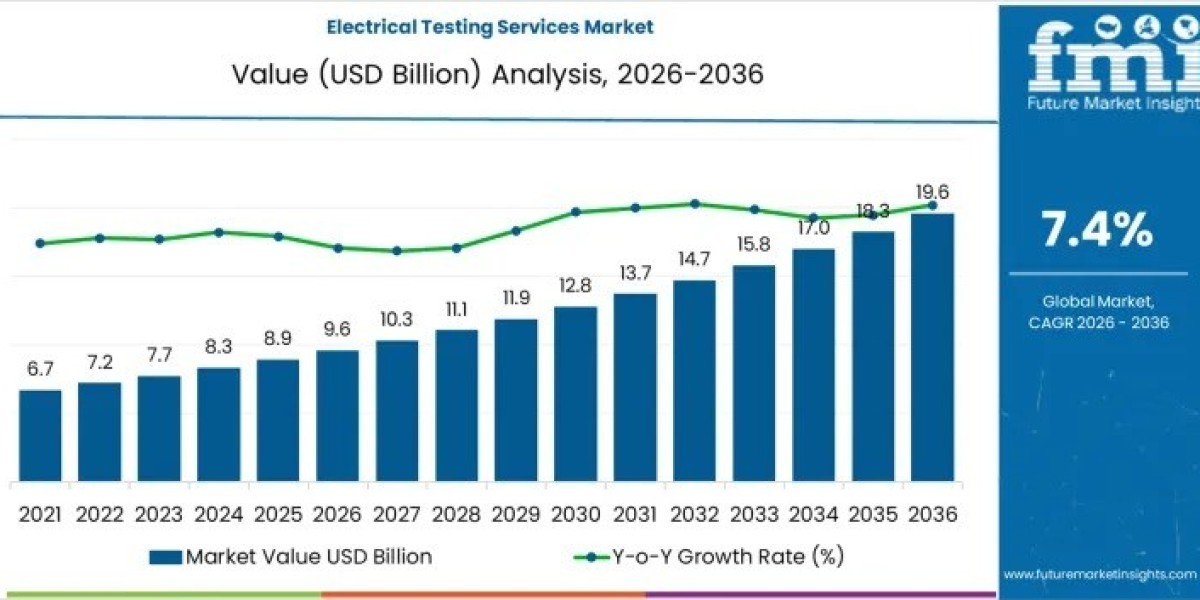

The global Electrical Testing Services Market is entering a decisive growth phase as industries prioritize operational safety, regulatory compliance, and predictive maintenance. Valued at USD 9.6 billion in 2026, the market is projected to reach USD 18.2 billion by 2036, expanding at a CAGR of 7.40%. This momentum reflects a structural shift away from reactive inspections toward systematic, data-backed testing across power generation, transmission and distribution (T&D), industrial facilities, and commercial infrastructure.

Electrical systems are becoming more complex as electrification, automation, and digital monitoring accelerate. In parallel, regulators are tightening safety and performance standards. Together, these forces are pushing electrical testing services from a discretionary expense to a core operational requirement across critical sectors.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-6683

Why Electrical Testing Services Are Becoming Mission-Critical

Historically, electrical testing was performed during commissioning or after failures occurred. Today, preventive and predictive testing is essential to minimize downtime, reduce safety risks, and extend asset life. Modern service portfolios now include:

- Motors and generator testing

- Transformer and circuit breaker testing

- Protection and relay testing

- Battery and backup power testing

- Rotating equipment vibration analysis

- Thermographic inspections

Cost structures are shaped by specialized diagnostic equipment, certified personnel, and strict compliance requirements. As a result, margin concentration favors providers offering integrated, multi-service portfolios and advanced data interpretation rather than single-point testing.

Growth Trajectory: Volume-Driven Expansion With Premium Service Upside

Between 2026 and 2031, the market is expected to grow from USD 9.6 billion to USD 13.2 billion, adding USD 3.6 billion in value. Roughly 65% of this growth is volume-led, supported by infrastructure expansion and industrial automation, while 35% comes from pricing gains tied to advanced diagnostics and compliance services.

From 2031 to 2036, expansion accelerates further, with the market adding USD 5.0 billion to reach USD 18.2 billion. Volume remains the primary driver, but premium services—such as predictive analytics, digital reporting, and long-term service contracts—strengthen revenue stability for leading providers.

Motors and Generator Testing Leads by Service Type

Motors and generator testing accounts for approximately 25% of total service demand, making it the largest service category. These assets are central to continuous industrial operations and power generation, where failures can trigger significant financial and safety consequences. Testing focuses on insulation resistance, partial discharge, vibration analysis, and performance diagnostics to identify early signs of degradation.

Regulatory requirements and the high replacement cost of rotating equipment reinforce consistent demand, particularly in power stations, data centers, and heavy manufacturing.

Data Centers Dominate End-Use Demand

Data centers represent nearly 25% of total end-use demand, positioning them as the single largest customer group. With zero tolerance for power interruptions, data center operators rely on frequent and predictive electrical testing to ensure uptime, protect sensitive equipment, and meet compliance obligations.

Testing programs in data centers extend across generators, transformers, switchgear, and backup systems, making this segment both high-value and service-intensive.

Regional Growth Patterns Highlight Asia’s Momentum

Demand growth varies by region, shaped by industrialization, infrastructure investment, and regulatory enforcement:

- India (8.1% CAGR): Rapid industrialization, grid expansion, and renewable integration drive strong demand for certified testing services.

- China (7.7% CAGR): Large-scale infrastructure and manufacturing growth increase the need for standardized electrical diagnostics.

- United Kingdom (7.1% CAGR): Workplace safety regulations and infrastructure upgrades sustain steady adoption.

- Germany (6.7% CAGR): Industrial electrification and automation fuel demand for advanced testing methodologies.

- United States (6.4% CAGR): Infrastructure modernization and preventive maintenance programs underpin stable growth.

Competitive Landscape: Scale and Integration Define Advantage

The market remains fragmented at regional levels, but scale and service breadth create clear competitive advantages. Global players such as Schneider Electric, Siemens AG, Eaton Corporation plc, General Electric Company, and ABB Inc. differentiate through integrated testing, engineering expertise, and compliance assurance.

Mid-sized and regional specialists—including Power Products & Solutions, American Electrical Testing, Haugland Group LLC, Dekra, and others—compete on responsiveness, localized expertise, and niche capabilities. Firms lacking certified personnel or multi-service offerings face slower adoption and margin pressure, while integrated providers secure long-term contracts and recurring revenue.

Technology and Partnerships Reshape Service Delivery

Advanced diagnostics, IoT-enabled monitoring, and automated reporting are redefining electrical testing services. Collaboration between service providers, equipment manufacturers, and facility operators improves testing accuracy and minimizes operational disruption. Digital recordkeeping and predictive analytics are becoming standard expectations, not optional enhancements.

Strategic Outlook Through 2036

By 2036, electrical testing services are expected to be embedded into standard asset management practices across industrial, commercial, and utility sectors. Growth will favor providers that combine certified expertise, digital capabilities, and comprehensive service portfolios aligned with regulatory and safety priorities.