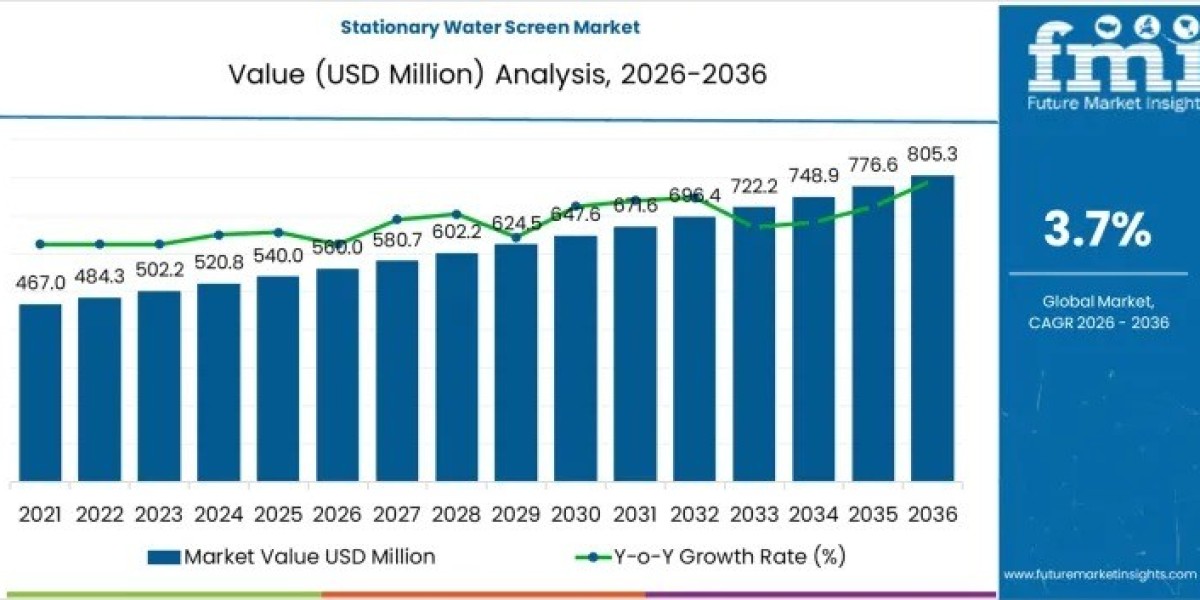

The Stationary Water Screen Market is projected to reach USD 560.0 million in 2026 and expand to USD 805.3 million by 2036, registering a CAGR of 3.7% over the forecast period. Market value is anchored in fixed intake protection requirements across power generation, municipal water supply, and industrial abstraction systems.

Unlike configurable filtration equipment, stationary water screens are permanent structural installations. Demand formation is therefore governed by intake count, hydraulic load, debris exposure, and regulatory compliance rather than short-term utilization or replacement cycles. Once installed, substitution is limited, reinforcing long-term revenue stability.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-30871

Revenue Drivers: Compliance, Refurbishment, and Intake Expansion

Revenue progression in the stationary water screen market reflects incremental infrastructure expansion, refurbishment of aging intake structures, and compliance-driven retrofits. Environmental regulations governing entrainment limits, intake velocity, and aquatic protection are increasing engineering specificity, pushing buyers toward customized designs.

Public procurement cycles and EPC-led project structures continue to moderate spending cadence, while replacement demand emerges from corrosion fatigue, structural deformation, and capacity mismatch under changing flow conditions.

Key revenue contributors include:

- Aging municipal and industrial intake refurbishment

- Power plant cooling water intake protection

- Regulatory-driven intake upgrades

- Lifecycle replacement of corroded screening assets

Why Demand for Stationary Water Screens Is Rising

Stationary water screens play a critical role in protecting pumps, pipelines, heat exchangers, and treatment equipment from debris and solids. Their passive operation ensures uninterrupted flow while minimizing mechanical failure risks.

Engineers specify stationary screens based on:

- Structural strength and corrosion resistance

- Bar spacing tolerance aligned with site hydrology

- Hydraulic stability and low head loss

- Long-term serviceability and maintenance access

Regulatory requirements further reinforce adoption by mandating intake designs that reduce harm to aquatic organisms while maintaining target abstraction volumes.

Screen Type Trends: Fixed Bar Screens Lead Demand

Fixed bar screens account for the largest demand share at 36.0%, driven by their mechanical simplicity and reliability. These screens intercept coarse debris using rigid bar spacing and operate without moving parts, reducing maintenance dependency.

Screen type insights:

- Fixed bar screens dominate high-flow, debris-variable environments

- Wedge-wire screens serve finer separation requirements

- Coarse trash racks address heavy debris loads

Preference remains skewed toward durable, low-complexity designs that support long service life under continuous immersion.

Application Analysis: Raw Water Intakes Dominate

Raw water intake applications represent 34.0% of total demand, making them the largest application segment. These installations protect upstream systems supplying untreated water to municipal, industrial, and power facilities.

Application-driven demand factors:

- Continuous intake reliability requirements

- Prevention of pump and equipment damage

- Stable hydraulic performance under variable debris loads

Wastewater headworks and industrial process water systems contribute secondary demand, but intake protection remains the primary deployment point.

Material Selection: Durability Drives Specification

Stainless steel accounts for 48.0% of material demand, reflecting its superior corrosion resistance, mechanical strength, and fabrication flexibility. Continuous exposure to water, chemicals, and biological fouling makes durability a critical procurement criterion.

Material preference highlights:

- Stainless steel for longevity and strength

- Coated carbon steel for cost-sensitive applications

- FRP and composites for lightweight, low-load environments

Material selection directly influences lifecycle cost and maintenance planning.

Global Demand Outlook: Steady Expansion Across Emerging Markets

Demand for stationary water screens is expanding globally as infrastructure operators prioritize intake reliability and compliance.

Fastest-growing countries include:

- India: 4.8% CAGR

- China: 4.4% CAGR

- Indonesia: 4.3% CAGR

- Brazil: 4.0% CAGR

- Mexico: 3.7% CAGR

India’s growth is supported by riverine and canal-based abstraction, thermal power cooling requirements, and monsoon-driven debris variability. China sustains demand through industrial intake protection and urban utility modernization. Growth across regions reflects operational necessity rather than discretionary investment.

Competitive Landscape: Engineering and Lifecycle Support Matter

Competition in the stationary water screen market centers on engineered reliability, corrosion resistance, and long-term service support. Buyers prioritize suppliers capable of delivering customized screening solutions that meet hydraulic performance and environmental standards.

Key players include:

- Huber SE

- Aqseptence Group

- WesTech Engineering

- ANDRITZ

- Xylem

- Veolia

- Parkson (Xylem)

- Jash Engineering

- Ovivo

- SUEZ

Differentiation increasingly depends on low-maintenance designs, automation compatibility, and lifecycle service capabilities.