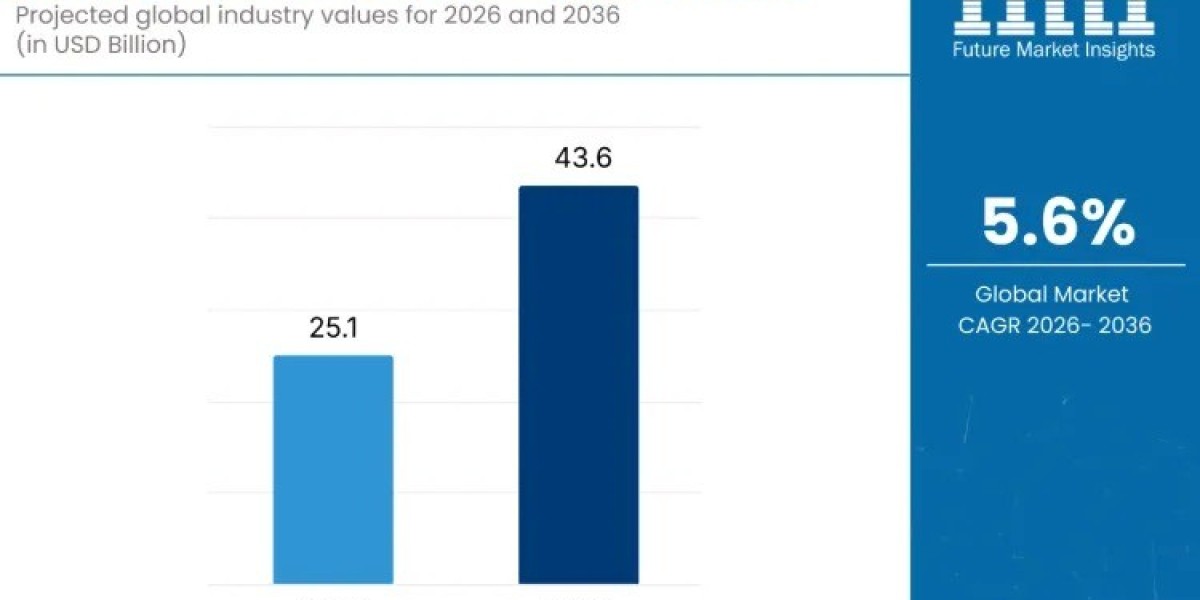

The Industrial Hose Assembly Market is entering a sustained growth phase as global industries prioritize reliable fluid and material transfer systems. Valued at USD 25.1 billion in 2026, the market is projected to reach USD 43.6 billion by 2036, expanding at a CAGR of 5.6%. This growth reflects the indispensable role hose assemblies play across manufacturing, oil and gas, chemicals, construction, automotive, agriculture, and mining operations, where performance, durability, and safety are non-negotiable.

Industrial hose assemblies are no longer viewed as interchangeable components. They are engineered solutions designed to handle extreme pressures, corrosive media, temperature fluctuations, and continuous-duty cycles. As industrial processes become more automated and regulated, demand is shifting toward high-quality, compliant hose systems that minimize downtime and operational risk.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-3751

Access to ongoing market intelligence is becoming essential as procurement cycles shorten and technology adoption accelerates. Year-round insights help stakeholders anticipate demand shifts, pricing dynamics, and regional opportunities.

Key Growth Drivers Supporting the 2026–2036 Outlook

Several structural factors are shaping the market’s upward trajectory:

- Infrastructure and industrial expansion: Large-scale construction, mining, and energy projects are increasing the need for heavy-duty hose systems.

- Material innovation: Advances in rubber compounds, thermoplastic elastomers, and reinforced metal hoses are extending service life and improving resistance to abrasion, chemicals, and heat.

- Regulatory compliance: Stricter environmental and safety regulations are pushing industries to replace aging hose systems with certified, leak-resistant assemblies.

- Maintenance and replacement cycles: Retrofit projects and preventive maintenance programs are generating recurring demand across mature industrial markets.

Together, these drivers reinforce the market’s resilience even amid fluctuations in raw material pricing.

Segment Insights: Where Demand Is Concentrated

Material leadership – Rubber dominates:

Rubber hose assemblies account for 57.4% of global demand in 2026 and retain leadership through 2036. Their flexibility, vibration tolerance, and abrasion resistance make them suitable for diverse applications, from construction sites to chemical processing plants. Plastics are gaining traction in lightweight and low-pressure uses, while metal hoses remain critical for extreme temperature and high-pressure environments.

Product preference – Medium pressure hoses lead:

Medium pressure hoses represent 46.8% of global demand in 2026. Their balance of performance, durability, and cost-efficiency supports widespread adoption in agriculture, food processing, material handling, and general manufacturing. This versatility secures their position as the most widely deployed product category.

Regional Dynamics: Growth Hotspots and Mature Markets

- North America remains a major consumption hub, supported by infrastructure upgrades and strong oil, gas, and chemical industries.

- Asia Pacific is the fastest-growing region, driven by manufacturing expansion in China, India, and Southeast Asia.

- Europe continues to focus on precision engineering, automation, and compliance-driven replacement demand.

Emerging economies are particularly influential as new industrial facilities prioritize modern hose systems from the outset.

Country-Level Momentum Shaping Global Demand

India leads with a projected CAGR of 6.8% through 2036, supported by rapid industrialization, infrastructure programs, and the “Make in India” initiative. China follows at 6.2%, fueled by construction, automation, and policy-backed industrial development. The United States records 5.5% growth, anchored in infrastructure modernization and energy sector requirements. Brazil (5.3%) benefits from mining and agricultural mechanization, while Germany (4.9%) leverages Industry 4.0 adoption and advanced manufacturing practices.

Industry Dynamics: Challenges and Emerging Trends

While growth prospects are strong, the market faces challenges such as volatile raw material prices, compliance complexity in hazardous material handling, and shortages of skilled installation and maintenance labor. These constraints are encouraging manufacturers to focus on standardized, pre-assembled hose solutions that reduce installation errors and downtime.

Key trends reshaping the industry include:

- Adoption of smart and IoT-enabled hoses for predictive maintenance

- Rising demand for customized assemblies tailored to specific processes

- Increased focus on sustainable and eco-friendly materials

These trends signal a shift toward higher-value, technology-integrated offerings.

Competitive Landscape: Innovation as a Differentiator

The market is moderately consolidated, with leading players such as Gates Corporation, Parker Hannifin Corp., Continental AG, Eaton Corporation Plc., and Trelleborg AB holding significant share. Competition centers on material expertise, R&D investment, and the ability to deliver integrated hose solutions with global service support. Regional and niche players are gaining ground through customization and localized manufacturing strategies.