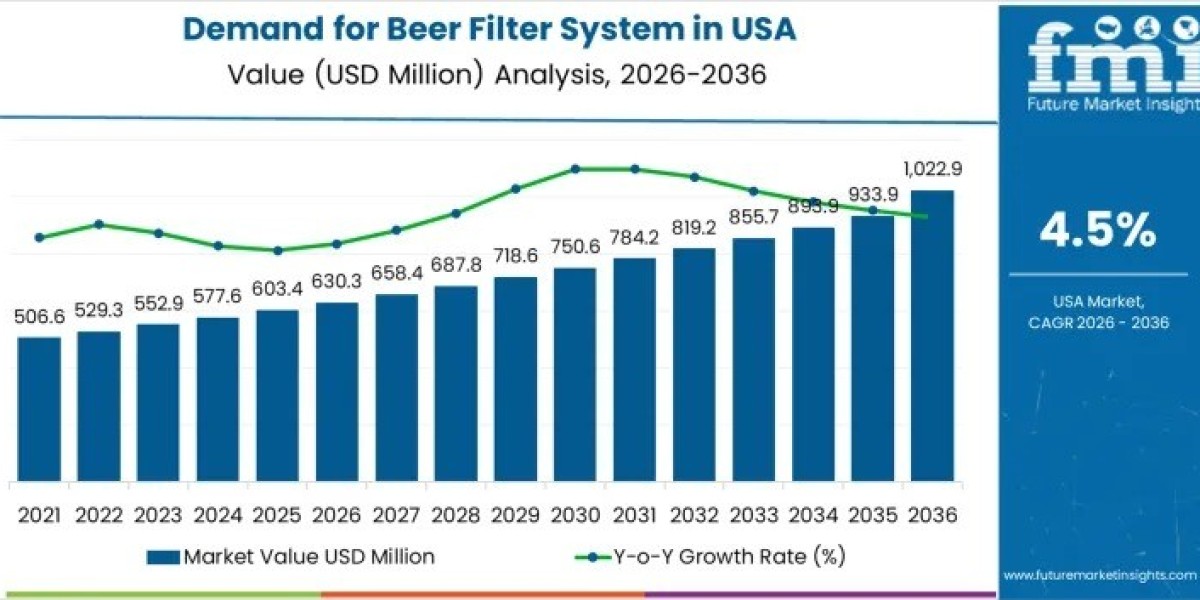

The Demand for Beer Filter System in USA is on a consistent growth trajectory as breweries invest in advanced filtration to meet rising expectations for clarity, stability, and flavor consistency. The market is valued at USD 630.3 million in 2026 and is forecast to reach USD 1,022.9 million by 2036, expanding at a 4.5% CAGR over the forecast period.

Growth remains gradual in the early years as breweries optimize existing production lines. By 2031, market demand is projected to reach USD 750.6 million, after which adoption accelerates due to increased capacity expansions, packaging growth, and technology upgrades across the USA brewing industry.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-29941

Key Market Highlights at a Glance

- Market value (2026): USD 630.3 million

- Forecast value (2036): USD 1,022.9 million

- CAGR (2026–2036): 4.5%

- Leading equipment type: Plate filters

- Dominant application: Kieselguhr filtration

- High-growth regions: West USA, South USA

Why Demand for Beer Filter Systems Is Rising in the USA

Beer filtration is essential for removing yeast, proteins, and haze-forming particles that impact visual appeal and shelf stability. As USA breweries expand beyond taproom sales into regional and national distribution, filtration has become a critical quality control step.

Key growth drivers include:

- Rising consumer preference for clear, visually appealing beer

- Expansion of craft and microbreweries across multiple states

- Increasing emphasis on batch-to-batch consistency

- Stricter distributor and retailer quality requirements

Sustainability concerns are also influencing purchasing decisions, with breweries seeking filtration solutions that minimize waste, improve water efficiency, and reduce operating costs.

Technology Advancements Accelerating Adoption

Technological innovation is reshaping the beer filtration landscape. Modern systems offer higher efficiency while preserving beer flavor and aroma—historically a concern for craft brewers.

Notable technology trends include:

- Cross-flow and membrane filtration for enhanced clarity

- Automation and digital controls to reduce labor dependency

- Compact and modular systems suitable for small breweries

- Improved cleaning-in-place (CIP) designs lowering maintenance time

These advancements are making high-quality filtration more accessible, especially for small and mid-sized breweries previously limited by capital constraints.

Plate Filters Lead Equipment Demand

Plate filters account for approximately 45% of total demand in the USA beer filter system market. Their dominance is supported by proven reliability, high throughput capacity, and compatibility with traditional filtration processes.

Plate filters are preferred because they:

- Handle large production volumes efficiently

- Offer lower operational costs compared to alternatives

- Deliver consistent beer clarity and stability

- Integrate easily with kieselguhr filtration systems

As breweries continue to prioritize scalable and cost-effective solutions, plate filters are expected to retain their leadership position through 2036.

Kieselguhr Filtration Remains the Primary Application

Kieselguhr filtration represents nearly 55% of application demand in the USA market. Diatomaceous earth remains a trusted filtration medium due to its effectiveness in removing yeast and suspended solids without altering flavor.

Key factors supporting kieselguhr dominance include:

- High efficiency in beer clarification

- Cost-effectiveness for large-scale operations

- Compatibility with both craft and commercial breweries

Despite the emergence of alternative technologies, kieselguhr filtration continues to play a central role in mainstream beer production.

Regional Demand Outlook Shows Strong West and South Performance

Regional analysis highlights uneven but positive growth across the USA:

- West USA (5.1% CAGR): Driven by strong craft beer clusters in California, Oregon, and Colorado, with a focus on premium quality and sustainability.

- South USA (4.6% CAGR): Growth supported by expanding craft breweries in Texas, Florida, and Georgia, where filtration is critical for shelf life in warmer climates.

- Northeast USA (4.1% CAGR): Mature beer culture emphasizes consistency and visual quality in packaged beer.

- Midwest USA (3.6% CAGR): Stable growth supported by traditional brewing hubs and rising sustainability investments.

Competitive Landscape and Strategic Positioning

The USA beer filter system market is characterized by technology-driven competition and service differentiation. Leading players such as Krones AG, ZIEMANN International GmbH, Koruntec International GmbH, 3M Europe, and Criveller focus on performance reliability, automation, and tailored system designs.

Manufacturers are increasingly offering customized solutions to address brewery-specific challenges, including haze control, throughput optimization, and operational efficiency.

Market Outlook Through 2036

By 2035, market demand is projected to approach USD 893.9 million, before surpassing the USD 1 billion threshold in 2036. This acceleration underscores filtration’s transition from optional processing equipment to a strategic investment aligned with long-term brewery competitiveness.