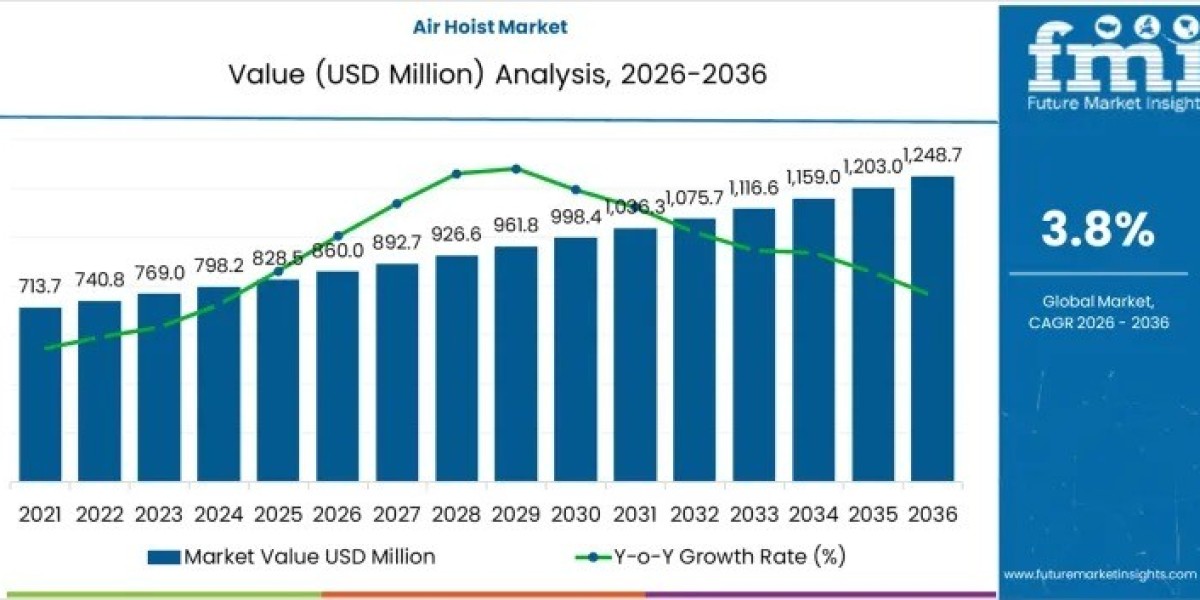

The Air Hoist Market is positioned for consistent expansion through 2036, supported by rising industrial safety standards and demand for reliable lifting solutions in harsh and hazardous environments. The market is valued at USD 860 million in 2026 and is projected to reach USD 1,248.7 million by 2036, registering a CAGR of 3.8% during the forecast period.

This growth reflects structural demand rather than cyclical volatility. Air hoists remain essential across industries where electric lifting systems pose ignition or reliability risks, including oil and gas, chemical processing, shipbuilding, mining, and heavy manufacturing. As industrial operators place greater emphasis on safety-certified equipment and predictable performance, pneumatic lifting technologies continue to secure long-term relevance.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-30980

Market Size Snapshot and Growth Indicators

Key data points highlight the market’s steady upward trajectory:

- Market value in 2026: USD 860 million

- Forecast value by 2036: USD 1,248.7 million

- Global CAGR (2026–2036): 3.8%

- Leading hoist type: Pneumatic chain hoists (62% share)

- Dominant capacity segment: 1–3 tons (46% share)

- Fastest-growing country market: India (4.9% CAGR)

These figures underline the market’s role as a foundational component of industrial material handling rather than a discretionary capital purchase.

Production Concentration and Supply Chain Dynamics

Manufacturing in the air hoist market is concentrated among a limited number of global players, enabling economies of scale and standardized quality benchmarks. However, this concentration also introduces exposure to supply chain risks, including raw material shortages, logistics disruptions, and geopolitical uncertainty.

To mitigate these challenges, manufacturers are increasingly focusing on:

- Regional production hubs to shorten lead times

- Supplier diversification to reduce dependency risks

- Flexible manufacturing systems that support demand variability

Over the next decade, supply chain resilience will become a competitive differentiator alongside product performance.

Five-Year Growth Block Analysis Through 2036

The air hoist market demonstrates predictable, phased expansion:

- 2026–2028: Early-stage growth driven by replacement demand and incremental adoption in manufacturing and construction, reaching approximately USD 926.6 million.

- 2028–2032: Accelerated uptake in automotive, heavy fabrication, and MRO-intensive industries, with market value approaching USD 1,036.3 million.

- 2032–2036: Sustained growth to USD 1,248.7 million, supported by industrial expansion in emerging economies and continued safety investments in mature markets.

This progression highlights long-term stability rather than speculative growth.

Key Demand Drivers Shaping the Market

Several structural factors are supporting market expansion:

- Increased emphasis on workplace safety and explosion-proof equipment

- Growth in oil and gas, mining, maritime, and heavy manufacturing sectors

- Preference for lifting systems that perform reliably under extreme conditions

- Rising adoption of compressed air infrastructure in industrial facilities

Air hoists continue to be favored where durability, controllability, and minimal electrical risk are operational priorities.

Segment Insights: Hoist Type and Capacity

By Hoist Type

- Pneumatic chain hoists dominate with a 62% market share due to versatility, ease of operation, and suitability for hazardous environments.

- Their precise load control and low maintenance requirements support widespread use across automotive and industrial assembly operations.

By Capacity

- The 1–3 tons segment leads with a 46% share, reflecting strong demand for medium-duty lifting solutions.

- This range offers an optimal balance of lifting power and efficiency for manufacturing, aerospace, and material handling applications.

Regional Trends and Country-Level Momentum

While North America and Europe remain mature markets, Asia Pacific is emerging as the primary growth engine.

- India: Leading growth at a 4.9% CAGR, driven by industrialization, infrastructure development, and safety-focused manufacturing upgrades.

- Indonesia and Saudi Arabia: Growth supported by expanding construction, energy, and industrial sectors.

- Mexico and Brazil: Adoption driven by manufacturing expansion and demand for safe, non-electric lifting systems.

These regions collectively reinforce the market’s global growth profile.

Competitive Landscape and Strategic Focus

The air hoist market is led by established players including Ingersoll Rand, KITO Corporation, Columbus McKinnon, J.D. Neuhaus, Harrington Hoists, Konecranes, Red Rooster Lifting, Demag (Terex MH), and Yale Hoists. Competition centers on reliability, safety certifications, customization, and lifecycle service support.

Strategic priorities across leading manufacturers include:

- Enhancing ergonomic and braking systems

- Improving durability for harsh environments

- Offering modular designs to reduce downtime

- Integrating monitoring features to support preventive maintenance

Outlook: Stability Anchored in Industrial Necessity

The air hoist market’s outlook through 2036 reflects disciplined growth rooted in operational necessity. While alternative lifting technologies continue to evolve, air hoists retain a defensible position where safety, reliability, and environmental tolerance are critical.