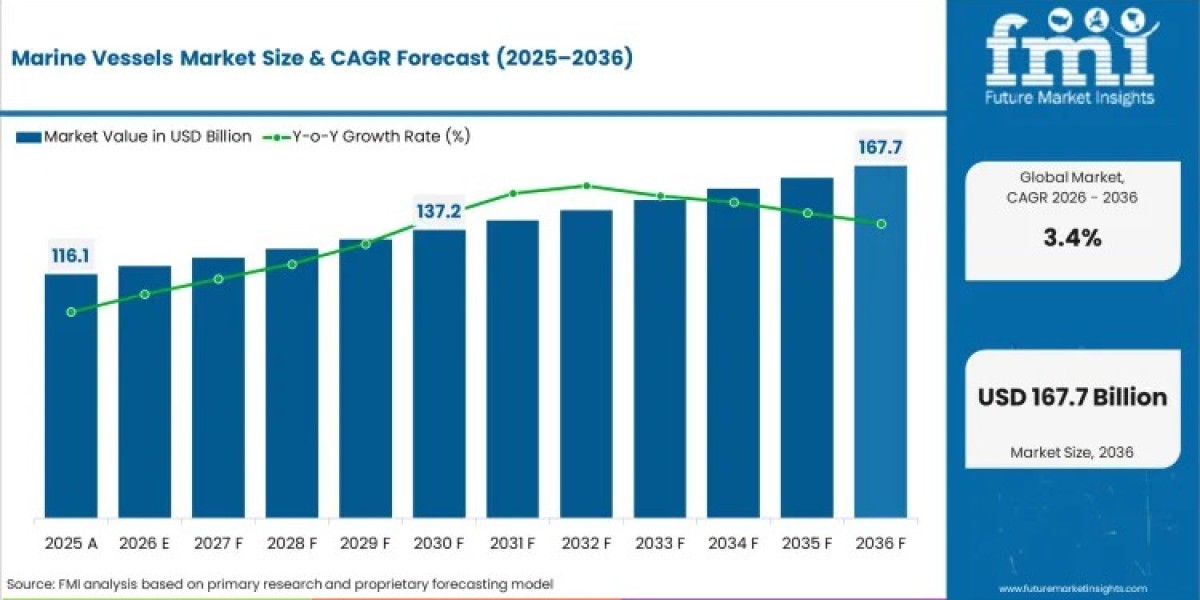

the global marine vessels market is entering a new era of steady, regulation-driven growth, underpinned by rising seaborne trade, naval modernization programs, and accelerating decarbonization mandates. According to Future Market Insights (FMI), the market is valued at USD 116.00 billion in 2025, expected to reach USD 120.05 billion in 2026, and projected to expand to USD 167.71 billion by 2036, registering a CAGR of 3.4% during the forecast period.

As global supply chains diversify and maritime logistics remain the backbone of international trade, vessel procurement cycles are increasingly shaped by fleet age, environmental compliance timelines, and geopolitical priorities.

Get detailed market forecasts, competitive benchmarking, and pricing trends: https://www.futuremarketinsights.com/reports/sample/rep-gb-24599

Featured Snippet: Key Market Insights

- What is the size of the marine vessels market in 2026?

USD 120.05 billion - What is the projected market value by 2036?

USD 167.71 billion - What is the CAGR (2026–2036)?

3.4% - What is driving growth?

Global trade expansion, IMO decarbonization mandates, and naval fleet modernization - Which segment dominates?

Commercial vessels with ~90% market share

Quick Stats: Marine Vessels Market

- Market Size (2025): USD 116.00 Billion

- Market Size (2026): USD 120.05 Billion

- Forecast Value (2036): USD 167.71 Billion

- CAGR (2026–2036):4%

- Incremental Opportunity: USD 47.66 Billion

Market Overview: A Capital-Intensive Industry Anchored in Global Trade

The marine vessels market remains a capital-intensive industrial sector, where demand is closely tied to:

- Global seaborne trade volumes

- Fleet aging and replacement cycles

- Naval defense recapitalization

- Environmental regulations under IMO frameworks

Commercial vessels—including bulk carriers, container ships, tankers, and gas carriers—continue to form the backbone of global logistics, accounting for the majority of newbuild demand.

Key Growth Drivers

- Expansion in Global Seaborne Trade

Rising international trade volumes are sustaining long-term demand for cargo vessels. Increasing containerization, energy transportation needs, and supply chain expansion are driving consistent shipbuilding activity.

- IMO Decarbonization Mandates

Regulations such as Carbon Intensity Indicator (CII) and Energy Efficiency Existing Ship Index (EEXI) are accelerating fleet renewal. Shipowners are transitioning toward:

- LNG dual-fuel vessels

- Methanol-ready ships

- Energy-efficient hull designs

- Naval Fleet Modernization

Defense spending is rising globally, particularly across Asia and NATO-aligned nations. Investments in:

- Combat vessels

- Patrol ships

- Auxiliary fleets

are expanding shipyard order books.

- Offshore Energy and Exploration Growth

Demand for offshore support vessels is increasing due to:

- Oil & gas exploration

- Offshore wind energy projects

- Subsea infrastructure development

Key Market Trends

- Shift toward dual-fuel and alternative propulsion systems

- Integration of digital navigation and predictive maintenance

- Emergence of semi-autonomous and autonomous vessel technologies

- Growing investments in sustainable shipbuilding materials and designs

Despite the shift toward greener alternatives, internal combustion engines (ICE) continue to dominate, holding 85% share in 2026, due to reliability and established infrastructure.

Segment Analysis

By Vessel Type

- Commercial Vessels dominate with ~90% market share (2026)

- Driven by cargo transport, passenger movement, and resource logistics

By Propulsion Type

- Internal Combustion Engines (ICE) lead with 85% share

- Increasing adoption of dual-fuel and low-emission alternatives

By Control Mechanism

- Manual systems dominate with 94% share

- Preferred for reliability, cost-effectiveness, and operational control

Regional Insights

Top Growth Markets (CAGR 2026–2036)

- China – 4.6%

- India – 4.3%

- Germany – 3.9%

- France – 3.6%

- United Kingdom – 3.2%

- United States – 2.9%

- Brazil – 2.6%

Regional Highlights

- China leads global shipbuilding capacity and naval expansion

- India benefits from port modernization and defense initiatives like Sagarmala

- Europe specializes in cruise ships and offshore wind vessels

- United States focuses on naval upgrades and eco-friendly vessels

Competitive Landscape

The marine vessels market is highly competitive, with leading players focusing on technological innovation, sustainability, and scale efficiency.

Key Players

- China State Shipbuilding Corporation (CSSC)

- Hyundai Heavy Industries (HHI)

- Daewoo Shipbuilding & Marine Engineering (DSME)

- Samsung Heavy Industries

- Fincantieri

Meyer Werft