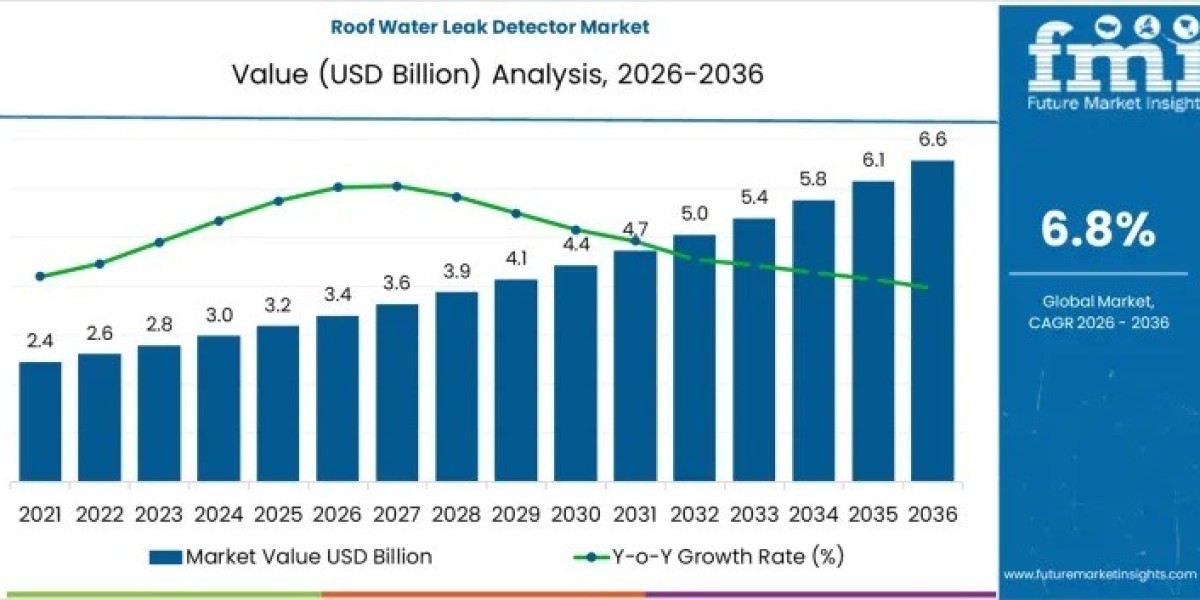

The Roof Water Leak Detector Market is projected to grow from USD 3.4 billion in 2026 to USD 6.6 billion by 2036, registering a CAGR of 6.8% over the forecast period. Market expansion reflects a structural shift in building maintenance strategies, where preventive monitoring systems are increasingly favored over reactive repairs.

Spending is concentrated in commercial and industrial properties with large roof surfaces, where undetected water intrusion can cause high secondary damage to interiors, equipment, and operations. Investment decisions are closely tied to lifecycle maintenance planning, insurance compliance, and long-term risk mitigation rather than discretionary technology upgrades.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates:

https://www.futuremarketinsights.com/reports/sample/rep-gb-18808

Key Growth Drivers

Several structural factors are supporting sustained demand for roof water leak detectors across global markets:

- Aging building infrastructure increasing vulnerability to moisture intrusion

- Rising insurance and compliance requirements encouraging preventive monitoring

- Higher awareness of lifecycle cost control among facility managers

- Climate variability leading to increased rainfall intensity and roof stress

Together, these drivers reinforce steady adoption across commercial, residential, and industrial building portfolios.

Cost and Deployment Dynamics

Market growth remains disciplined due to cost sensitivity and integration considerations. Installation complexity, system calibration needs, and long-term maintenance requirements influence procurement decisions. Integration with existing building management systems can extend deployment timelines, especially in retrofit projects.

False alarm risks caused by condensation or environmental exposure also affect ownership costs, making sensor reliability and durability critical evaluation criteria. As a result, buyers prioritize predictable loss prevention outcomes over rapid technology replacement cycles.

Product Type Trends

Smart roof water leak detectors account for 61.7% of global demand, reflecting strong preference for automated monitoring and real-time alert systems.

Key Points:

- Smart detectors enable continuous monitoring and remote alerts

- Integration with building management platforms improves response efficiency

- Adoption is highest in commercial and high-value residential properties

Conventional detectors retain 38.3% share, primarily in cost-sensitive installations and smaller facilities where advanced connectivity is not essential.

Connectivity Preferences

Connectivity choices reflect ease of installation and scalability requirements.

Key Points:

- Wireless systems lead with 54.2% share, driven by retrofit flexibility

- Reduced cabling supports deployment across complex roof structures

- Wired systems hold 45.8%, preferred in environments requiring stable connections

Wireless adoption is particularly strong in existing building stock, where infrastructure modifications are limited.

End-Use Segment Analysis

Commercial buildings represent the largest end-use segment, accounting for 36.0% of market demand.

Segment Highlights:

- Commercial: Office buildings, retail complexes, and mixed-use facilities prioritize uptime and tenant protection

- Residential: Represents 28.0%, supported by insurance awareness and preventive maintenance

- Industrial: Holds 26.0%, driven by protection of equipment and production continuity

- Warehouses: Account for 10.0%, focused on large roof area exposure

End-use distribution reflects varying risk tolerance and asset density across property types.

Regional Growth Outlook

Growth rates are strongest in regions with dense commercial infrastructure and regulatory maintenance enforcement.

Country CAGR Highlights:

- China: 7.1% – driven by large-scale commercial and industrial construction

- United States: 7.0% – supported by aging buildings and insurance-led adoption

- India: 6.8% – influenced by monsoon exposure and expanding commercial real estate

- United Kingdom: 6.3% – shaped by aging infrastructure and flat roof prevalence

- Brazil: 6.1% – supported by humidity, rainfall, and logistics facility expansion

Regional demand aligns more closely with asset protection priorities than with new construction volumes.

Competitive Landscape

The market is moderately consolidated, with competition centered on sensor accuracy, integration capability, and global service coverage.

Leading Participants Include:

- Honeywell International

- Siemens

- Johnson Controls

- Schneider Electric

- Bosch Building Technologies

These companies leverage broader building automation and smart infrastructure portfolios to embed leak detection within integrated facility management solutions.

Market Outlook

The roof water leak detector market is positioned for stable, long-term growth as preventive maintenance becomes a standard component of building risk management. While cost sensitivity and integration challenges remain, increasing climate exposure, aging infrastructure, and insurance-driven compliance continue to support sustained adoption across global property portfolios.