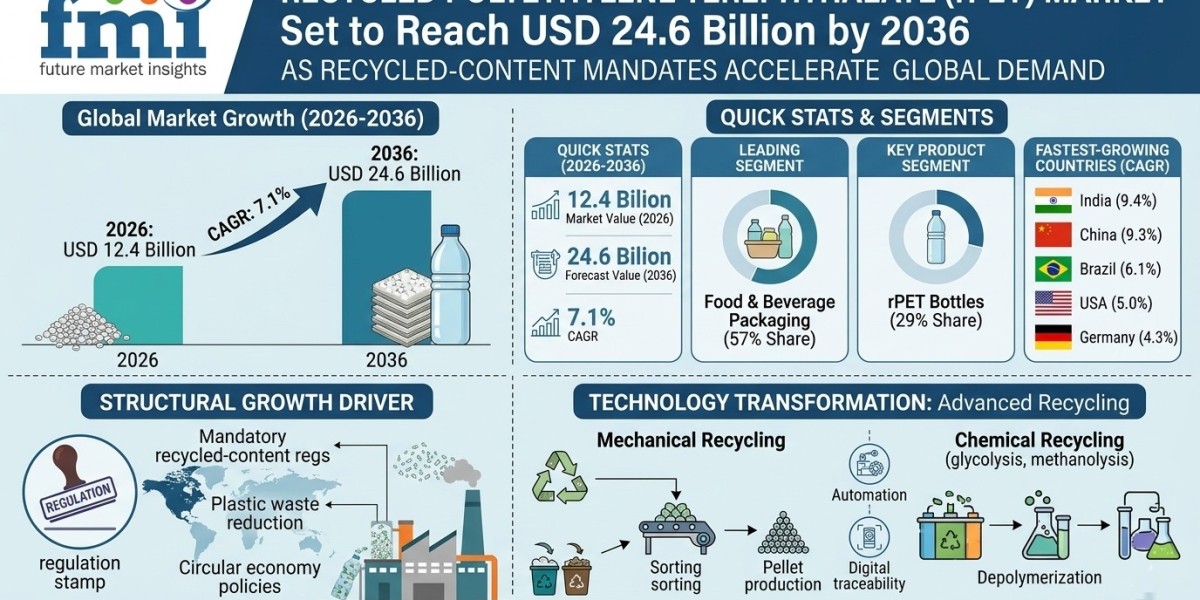

The global recycled polyethylene terephthalate (rPET) market is projected to witness strong expansion as regulatory mandates and circular economy policies reshape the plastics and packaging industry. The market is expected to increase from USD 12.4 Billion in 2026 to USD 24.6 Billion by 2036, registering a CAGR of 7.1% during the forecast period.

Quick Stats: Recycled Polyethylene Terephthalate (rPET) Market (2026–2036)

- Market Value (2026): USD 12.4 Billion ?????-??-??? ???? ????????? ??????

• Forecast Value (2036): USD 24.6 Billion

• CAGR: 7.1%

• Leading Segment: Food & Beverage Packaging – 57% market share

• Key Product Segment: rPET Bottles – 29% share

• Fastest-Growing Countries: India, China, Brazil, Germany, United States

• Key Growth Driver: Mandatory recycled-content regulations in packaging

Structural Growth Driver: Regulatory Mandates for Recycled Content

One of the most influential drivers shaping the rPET market is the implementation of binding recycled-content mandates in packaging regulations. Governments across Europe and North America are establishing minimum recycled-content requirements for plastic packaging, forcing companies to integrate recycled materials into their product supply chains.

Key regulatory and industry standards influencing the market include:

- Recycled-content mandates in plastic packaging

• Plastic waste reduction regulations

• Food-contact material safety certifications

• Circular economy and recycling policies

• Packaging sustainability compliance frameworks

From Compliance to Industry Transformation

The rPET industry is undergoing a structural transformation as recycling capacity scales from pilot projects to large industrial infrastructure. Major recycling companies are investing heavily in mechanical and chemical recycling facilities to meet rising demand from packaging manufacturers and global consumer brands.

The competitive landscape is evolving toward vertically integrated recycling ecosystems where companies control multiple stages of the value chain, including collection, sorting, processing, and resin production. This integration enables companies to secure feedstock supply while improving product quality and regulatory compliance.

At the same time, the market is witnessing a shift toward food-grade rPET, which commands a price premium due to strict safety and contamination control requirements in beverage and food packaging applications.

Key strategic priorities for companies include:

- Sustainability performance improvement

• Cost efficiency and recycling yield optimization

• High-quality food-grade recycled materials

• Supply chain traceability and compliance

• Vertical integration in recycling infrastructure

Technology Transformation: Advanced Recycling and Circular Materials

Technological innovation is playing a vital role in enabling high-quality recycled PET production. Mechanical recycling technologies remain the dominant method for producing rPET flakes and pellets from post-consumer PET bottles.

However, chemical recycling technologies such as glycolysis, methanolysis, and molecular depolymerization are emerging as transformative solutions capable of producing virgin-quality PET from difficult-to-recycle waste streams.

Digital traceability technologies are also being adopted to verify recycled-content claims and ensure regulatory compliance across the packaging supply chain.

Key innovation areas include:

- Advanced material recovery technologies

• Chemical recycling and molecular depolymerization

• Automation in sorting and recycling facilities

• Sustainable material engineering

• Digital traceability and certification systems

Segment Highlights

By Product Type

- rPET Bottles (29% share): Dominant segment due to established bottle-to-bottle recycling systems and large feedstock availability.

- rPET Flakes: Widely used in packaging, textile fibers, and sheet manufacturing applications.

- rPET Pellets and Chips: High-quality recycled resin used in packaging and industrial applications.

- Chemically Recycled rPET Resin: Emerging segment offering virgin-quality PET for high-performance applications.

- rPET Sheet and Film: Used in thermoforming packaging and industrial applications.

By Application / End Use

- Food & Beverage Packaging (57% share): Largest application driven by beverage bottle recycling and sustainability targets.

- Cosmetics Packaging: Increasing adoption of rPET in sustainable beauty product packaging.

- Pharmaceutical Packaging: Growing use of recycled materials in compliant packaging systems.

- Textile and Fiber: rPET used in polyester fiber production for apparel and industrial textiles.

- Sheet and Thermoforming Applications: Used in trays, containers, and rigid packaging formats.

Regional Outlook: Emerging Economies Drive Adoption

Global growth of the rPET market is shaped by regulatory leadership in Europe, recycling infrastructure expansion in North America, and rapid manufacturing growth across Asia Pacific. Europe leads the global market through strong policy frameworks, while Asia Pacific is witnessing increasing recycling capacity investments.

Country growth projections include:

- India (9.4% CAGR): Rapid expansion supported by government recycling policies and rising demand for sustainable packaging.

- China (9.3% CAGR): Government initiatives aimed at reducing plastic waste are driving recycling industry development.

- Brazil (6.1% CAGR): Growing packaging sector and improving recycling infrastructure support market expansion.

- Germany (4.3% CAGR): Advanced recycling systems and strong environmental regulations drive demand for rPET.

- United States (5.0% CAGR): Increasing recycling capacity and brand commitments to sustainable packaging.

Risk Landscape: Market Constraints and Challenges

Despite significant growth potential, the rPET market faces challenges related to feedstock availability, recycling infrastructure gaps, and quality consistency of recycled materials.

Key challenges include:

- Raw material feedstock shortages

• Supply chain disruptions in waste collection

• Infrastructure gaps in emerging economies

• Regulatory complexity across regions

• Quality consistency challenges in recycled materials

Competitive Landscape: Key Market Players

The rPET market is highly competitive with global recycling companies investing heavily in advanced technologies, recycling capacity, and strategic partnerships with consumer goods brands.

Leading companies operating in the market include:

- Indorama Ventures

• Plastipak Holdings, Inc.

• Veolia

• Eastman Chemical Company

• ALPLA Group

Other notable companies include Far Eastern New Century, CarbonLite Industries, Loop Industries, Biffa PLC, Verdeco Recycling Inc., and Placon Corporation.

Outlook: Future of the Recycled Polyethylene Terephthalate (rPET) Market

The long-term outlook for the rPET market remains highly positive as regulatory mandates, sustainability commitments, and circular economy initiatives accelerate demand for recycled plastics. Companies across the packaging and consumer goods sectors are expected to increase investments in recycling technologies and infrastructure.

Future growth drivers include:

- Technology advancement in recycling processes

• Sustainability initiatives and circular economy adoption

• Manufacturing expansion in recycling facilities

• Supply chain innovation and digital traceability

For an in-depth analysis of evolving industry trends and to access the complete strategic outlook for the market through 2036, visit the official report page at: https://www.futuremarketinsights.com/reports/recycled-polyethylene-terephthalate-packaging-market