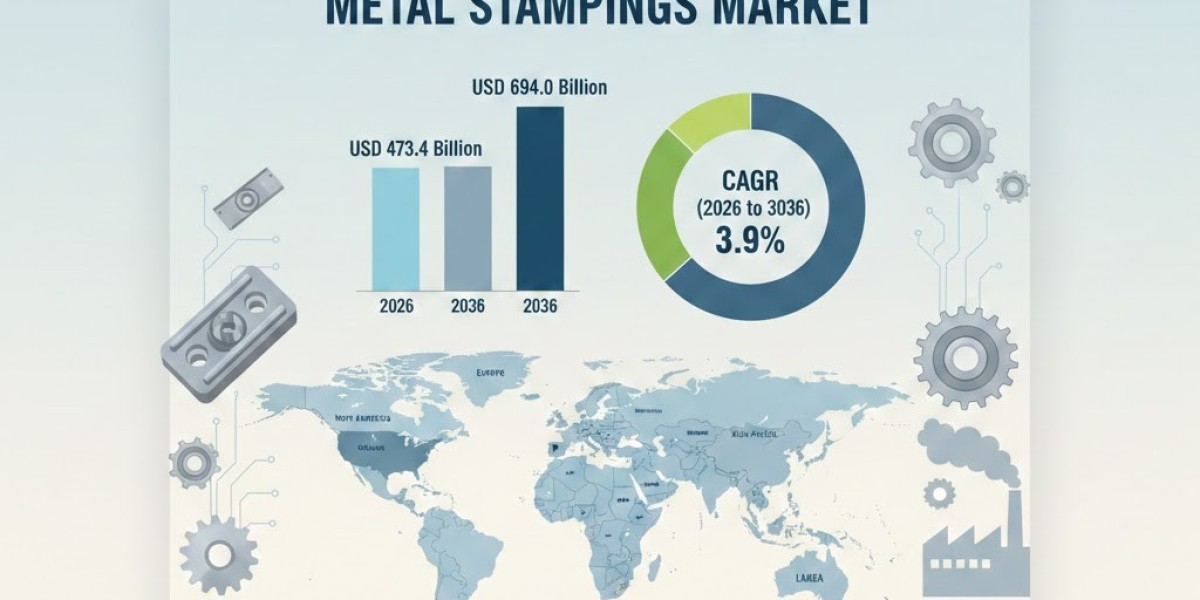

The global Metal Stampings Market is projected to grow from USD 473.4 billion in 2026 to USD 694.0 billion by 2036, expanding at a CAGR of 3.9%, according to Future Market Insights (FMI). The market’s steady rise reflects structural transformation across automotive electrification, consumer electronics miniaturization, defense modernization, and smart manufacturing adoption.

According to 2024 data published by the International Organization of Motor Vehicle Manufacturers, global vehicle production reached 93.5 million units, underscoring the substantial scale of automotive demand, which accounts for nearly 60% of total metal stamping consumption worldwide. This volume intensity is prompting stamping manufacturers to expand investments in advanced hot stamping presses, mega-stamping systems, and ultra-precision micro-stamping technologies to meet evolving performance and lightweighting requirements.

At the same time, shifting trade policies and tariff-induced cost pressures are accelerating supply chain localization, compelling OEMs to increasingly source stamped components from regional manufacturing partners to mitigate risk and maintain cost competitiveness.

Request For Sample Report | Customize Report | Purchase Full Report – https://www.futuremarketinsights.com/reports/sample/rep-gb-812

Market Valuation & Growth Outlook (2026–2036)

FMI’s proprietary forecasting model, built on vehicle production data, industrial metal consumption trends, and EV stamping content per vehicle analysis, indicates stable long-term expansion.

Key Data Highlights:

- 2026 Market Size: USD 473.4 Billion

- 2036 Forecast Value: USD 694.0 Billion

- CAGR (2026–2036): 3.9%

- Automotive Share: ~60% of total stamping demand

Global vehicle production reached 93.5 million units in 2024, as reported by the International Organization of Motor Vehicle Manufacturers, reinforcing automotive as the dominant consumption base for stamped components.

EV Transition Driving Structural Demand Shift

The automotive industry’s pivot to electric vehicles (EVs) is redefining stamping complexity and material requirements.

Stamped components are increasingly critical for:

- Battery enclosures using ultra-high-strength steel (UHSS)

- Crash-safety rails and structural reinforcements

- Lightweight aluminum body panels

- Motor housings and thermal management plates

Advanced processes such as hot stamping, mega-stamping, and servo-controlled blanking are replacing conventional progressive die systems to meet EV design standards.

Leading suppliers such as Gestamp Automoción, S.A. and Magna International Inc. are expanding EV-focused production lines globally, integrating automation and AI-powered inspection systems to enhance precision and reduce scrap rates.

Localization & Strategic Capacity Expansion

Supply chain regionalization is reshaping the competitive landscape, particularly in North America.

Recent developments include:

- John Deere announcing two new U.S. manufacturing facilities in 2026 to localize heavy equipment components.

- Ryerson acquiring Norlen Inc. to strengthen defense and agriculture stamping capabilities.

Tariff-driven cost pressures and geopolitical uncertainties are compelling OEMs to source regionally, increasing domestic stamping capacity investments.

Circular Steel & Low-Carbon Manufacturing Momentum

Sustainability is rapidly becoming a procurement prerequisite rather than a compliance checkbox.

In September 2025, Hydnum Steel partnered with Gestamp to convert stamping scrap into green hydrogen-based low-CO2 steel. Such circular supply chain integration is expected to become standard practice across Europe as Scope 3 emissions reporting intensifies.

Sustainability Trends Include:

- Scrap-to-steel recycling ecosystems

- Energy-efficient servo presses

- AI-driven predictive maintenance

- Reduced scrap rates (up to 30% efficiency gains in advanced blanking)

Process Innovation: Blanking & Embossing Lead

Blanking and embossing are gaining market traction due to precision and scalability benefits.

Blanking Advantages:

- High-speed production capability

- Superior edge quality

- Up to 30% material efficiency improvement

- Enhanced compatibility with AHSS

Embossing Growth Drivers:

- Functional grip textures in automotive interiors

- EMI shielding components in electronics

- Premium branding in consumer goods

- Heat dissipation designs for 5G infrastructure

Laser-assisted micro-stamping and digitally controlled ultra-precision embossing are expanding adoption in semiconductors and nano-electronics manufacturing.

Application Outlook: Automotive & Electronics Dominate

Automotive & Transportation

The largest revenue contributor, driven by:

- Lightweighting mandates

- EV platform scaling

- Structural safety reinforcement demand

- Hot stamping for crash-resistant frames

Stamped AHSS components enable 15%–25% vehicle weight reduction without structural compromise.

Consumer Electronics

Rapid miniaturization and durability requirements are accelerating micro-precision stamping demand.

Applications include:

- Smartphone and laptop casings

- Connectors and shielding components

- IoT and 5G infrastructure hardware

- Nano-scale electronic assemblies

Compared to plastic molding, stamping provides superior electromagnetic shielding and premium surface finishes.

Regional Growth Landscape

North America

- Strong automotive reshoring trends

- Aerospace recovery fueling demand

- Investment in CNC and IoT-enabled stamping lines

- Emphasis on sustainable manufacturing practices

Europe

- Carbon neutrality mandates driving low-carbon stamping

- EV production acceleration

- Adoption of hydroforming and precision metal forming

Asia-Pacific

- Fastest projected CAGR

- China’s EV manufacturing scale-up

- India’s infrastructure and “Make in India” initiatives

- Japan & South Korea’s automation leadership

Challenges & Strategic Opportunities

Challenges:

- Volatile steel, aluminum, and copper prices

- Supply chain disruptions

- Tooling wear and high setup costs

Opportunities:

- AI-powered defect detection

- Smart robotics integration

- Hybrid metal-composite forming

- EV and renewable energy infrastructure expansion

FMI analysts emphasize that the industry is shifting from commodity-driven volume production toward high-value, digitally integrated, sustainability-aligned manufacturing.